Amazon has long operated on razor-thin margins while reinvesting heavily in growth.

According to the analysis, Jeff Bezos’ playbook was to “sacrifice short-term returns to build scale”

. The

company’s real profit driver became AWS (cloud computing) – a “secret engine that quietly made more

profit than Amazon’s entire retail business combined”

. Under Andy Jassy’s leadership, Amazon flipped

the switch from growth to profit: it cut costs, raised prices on select services, and leaned on its

“absurdly profitable” cloud and advertising divisions . In just a few years the company swung from

losing money to reporting tens of billions in annual profits .

Amazon built immense scale with minimal profit for decades.

AWS and Advertising are now the core profit engines – both have much higher margins than retail.

Since Jassy became CEO, Amazon has aggressively cut costs and reined in spending while

boosting revenue from high-margin segments.

These strategic shifts underlie Amazon’s recent jump in profitability.

Historical Context: Growth over Profit

For roughly 20 years under Jeff Bezos, Amazon prioritized reinvestment and market share over nearterm profits. Bezos was willing to operate on “razor-thin margins and endless reinvestment”

, using debt

and reinvested cash rather than equity to fund growth. This approach built Amazon into a giant –

warehouses, logistics, AWS, entertainment, etc.

– but kept profits low. The turning point came when

Amazon Web Services (AWS) scaled up: AWS quietly became the profit engine. In fact, AWS generated

more profit than all of Amazon’s retail operations combined . This massive cash cushion enabled

Amazon to expand in new areas while deferring profits.

However, under Bezos (and until recently), Amazon deliberately delayed profitability. It reinvested in

faster shipping, Prime perks, hardware, and international expansion, often at the expense of margins. As

one summary puts it, Amazon’s historic playbook was to let “competitors’ margins become his

opportunity”

, focusing on scale first. Only now are the fruits of that strategy being harvested. ...

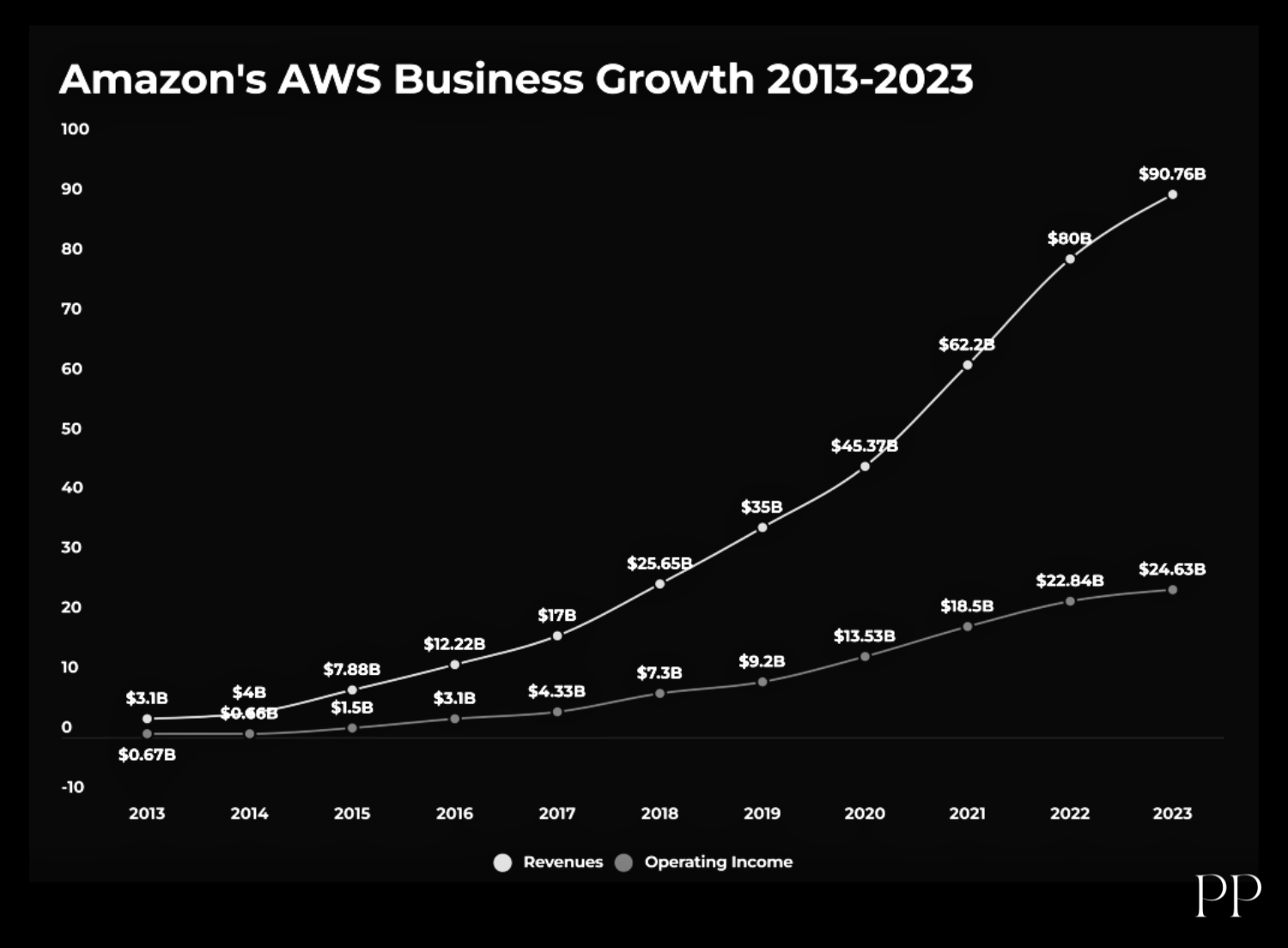

AWS: The Cloud Profit Engine

AWS’s growth and high margins are key to Amazon’s profitability story. In Q2 2025, AWS revenue was

$30.9 billion, up 17.5% year-over-year . Crucially, AWS has far higher operating margins than retail: AWS

operating income was $10.2 billion in that quarter (against $9.3B a year ago), reflecting roughly 33%

operating margin. By contrast, Amazon’s North America retail segment earned $100.1B in sales (11%

growth) but only $7.5B in operating profit . In other words, each dollar of AWS revenue translates to

much more profit than a dollar of retail.

Analysts note that AWS remains under strong demand. Goldman Sachs highlights AWS’s large backlog

and cost optimizations for AI workloads, forecasting the unit to sustain mid-30% operating margins into

2026. Thus AWS provides a steady, high-margin cash stream. AWS was “the secret engine” behind

Amazon’s turnaround.

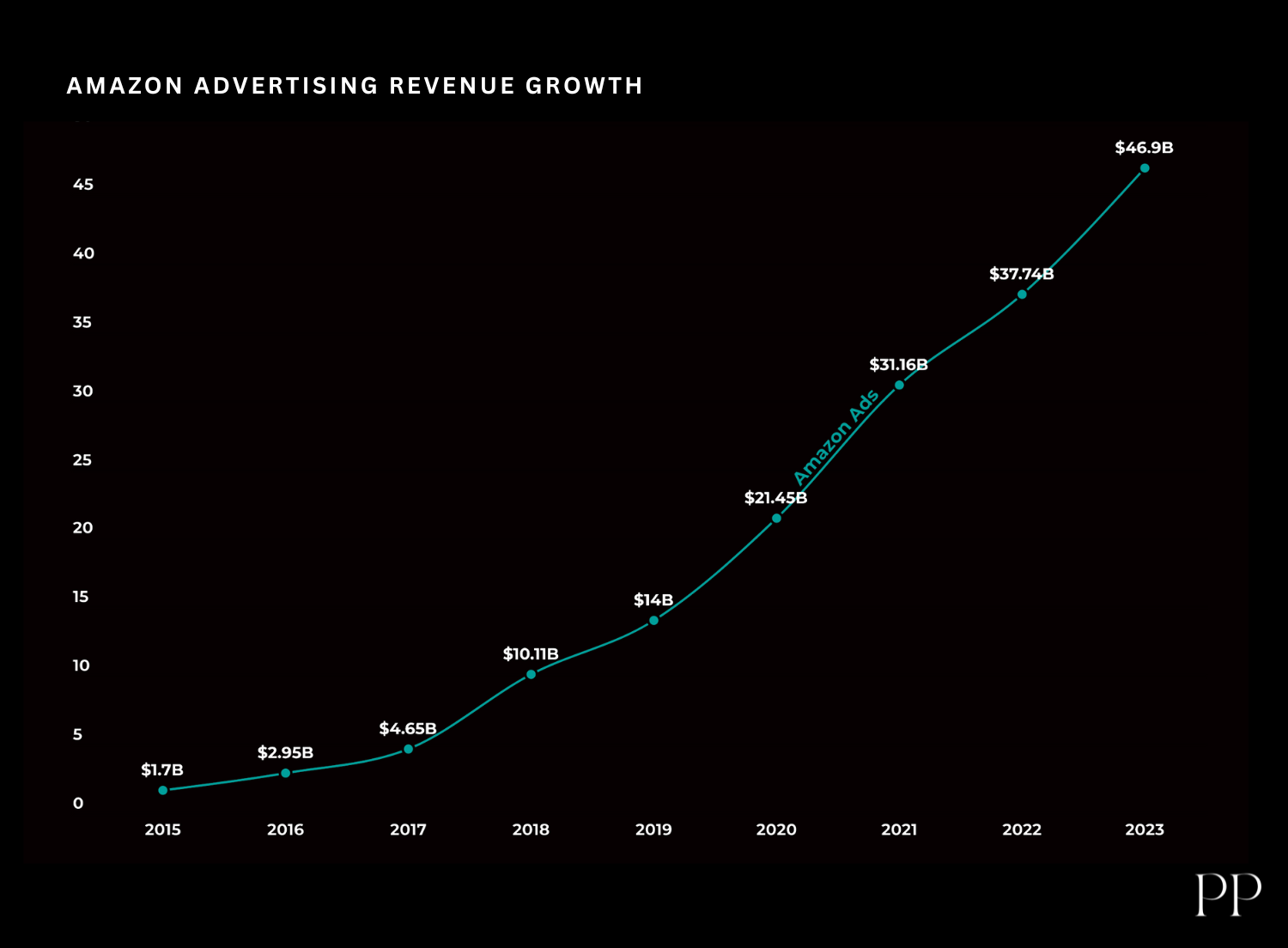

Advertising and Other High-Margin Segments

Amazon’s advertising business has likewise become hugely important. In Q2 2025, ads revenue hit

$15.7 billion, a 22% year-over-year jump . This makes it one of the fastest-growing parts of Amazon.

More importantly, advertising is extremely profitable: sponsored search, display ads, streaming ads and

other “retail media” carry operating margins around 60–70% (far higher than retail or even AWS).

Amazon has “leaned on its absurdly profitable … ad divisions” to boost the bottom line.

By way of scale, advertising now rivals a tech giant of its own: one analysis points out that if Amazon’s

ad unit had margins similar to Google’s, it would account for roughly 30% of Amazon’s total operating

profit. Broadly, ads and cloud are cited as quietly compounding profit drivers for Amazon . (For context,

other segments like subscription services and third-party seller services are growing steadily – e.g.

subscriptions hit $12.2B in Q2 – but they operate at lower margins.)

Cost Control and Pricing

In addition to leveraging AWS and ads, Amazon has also sharpened its cost control and taken advantage

of pricing power. Over the past few years it cut headcount, froze or slowed warehouse expansion, and

streamlined logistics – moves that trim operating expenses. specifically highlights that “Amazon cut

costs” under Jassy . (For example, Amazon announced layoffs of over 20,000 jobs in 2022–2023, and

scaled back new fulfillment centers.)

At the same time, Amazon has begun modest price increases. Its Prime membership fees have risen,

and it has passed through higher costs in some areas. While retail item prices were fairly stable as of

early 2025 , the company noted subtle price boosts and fees. In short, Amazon is no longer giving away

as much value for free.

“flipped the switch” by also “raising prices”

, relying less on promotions and

absorbing more costs into pricing . These moves expand margins on the core business.

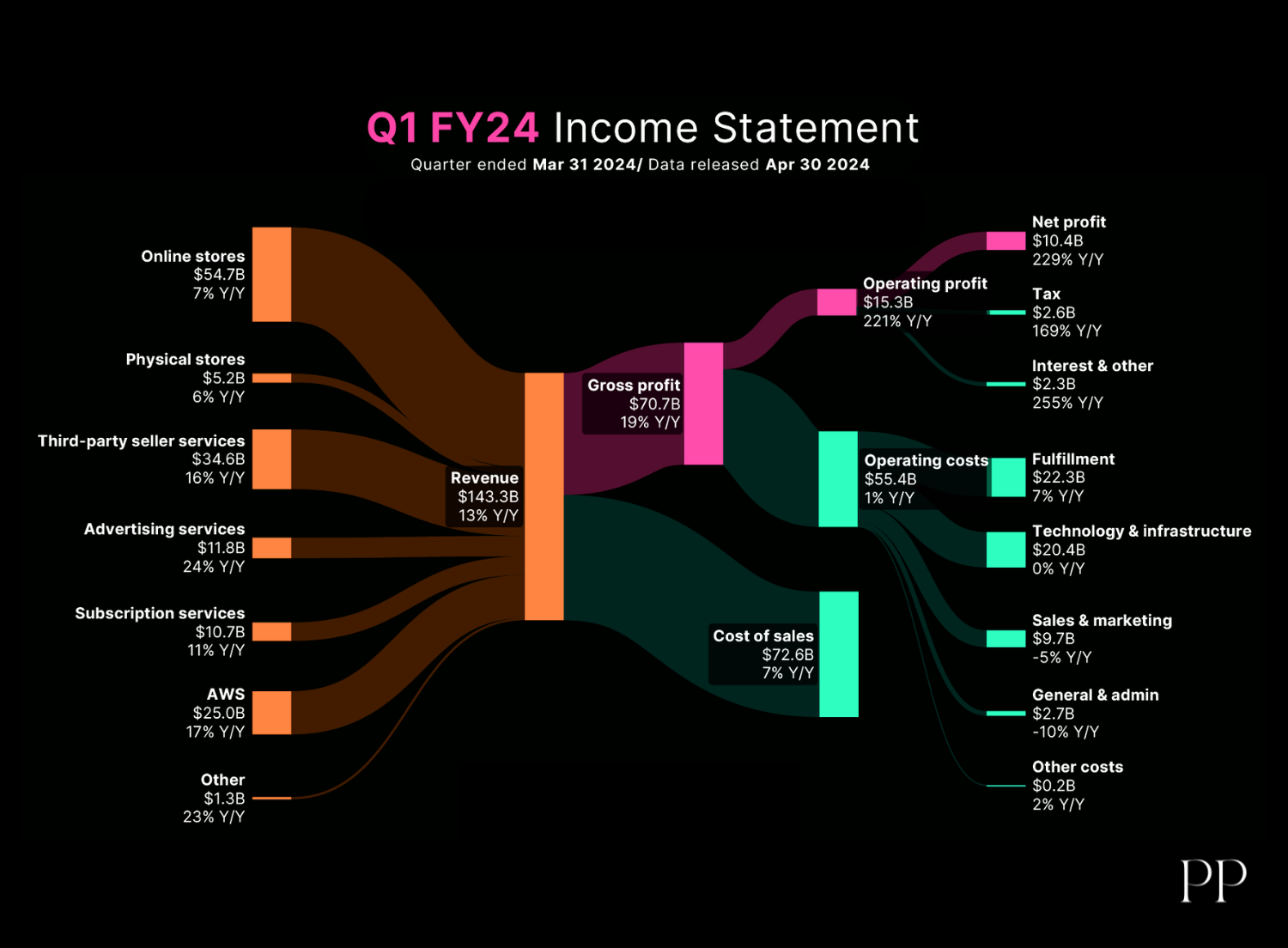

Recent Financial Results (Q2 2025)

The shift is evident in Amazon’s latest earnings. In Q2 2025 (ended June 30), net sales were $167.7

billion, up 13% year-over-year . Operating income jumped to $19.2 billion (vs. $14.7B in Q2 2024) . Net

income was $18.2 billion ($1.68 per share), compared to $13.5B ($1.26) a year earlier . Put differently,

Amazon’s net profit margin was about 10.5% in that quarter – far above the low single digits it typically

saw in previous years.

Key segment figures from that quarter include: - North America (retail) sales of $100.1B (+11%) with

$7.5B operating income .

International retail sales of $36.8B (+16%) with $1.5B operating income (vs. $0.3B prior year) .

AWS sales of $30.9B (+17.5%) with $10.2B operating income.

Advertising sales of $15.7B (+22%) (profit not separately disclosed, but margins are very high).

These results led analysts to sharply raise forecasts. For example, Goldman Sachs in October upgraded

Amazon citing AWS and ads as underappreciated profit drivers . Even Amazon’s own guidance for Q3

2025 shows high expectations: operating income was projected in the $15.5–$20.5B range, reflecting

continued strong profit generation .

Conclusion

In summary, the report’s argument is borne out by the facts: Amazon has finally realized robust profits

by shifting its focus away from perpetual reinvestment and toward its most lucrative businesses. AWS

and the ad unit are now pulling in huge revenue with outsized margins, and management has tightened

the belt elsewhere. The result is a historic profit surge – Amazon recorded its first-ever $18B+ quarter,

with net margins above 10% . As one commentator notes, Amazon has gone from “losing billions to

making $85 billion annually” in a few years . This marks a turning point: after two decades of accepting

low margins to build a global empire, Amazon is finally enjoying the financial payoff of that strategy.

Sources: The analysis is based on the Media commentary and Reports, expert opinions, supplemented by Amazon’s Q2 2025 earnings

release and financial press reports.