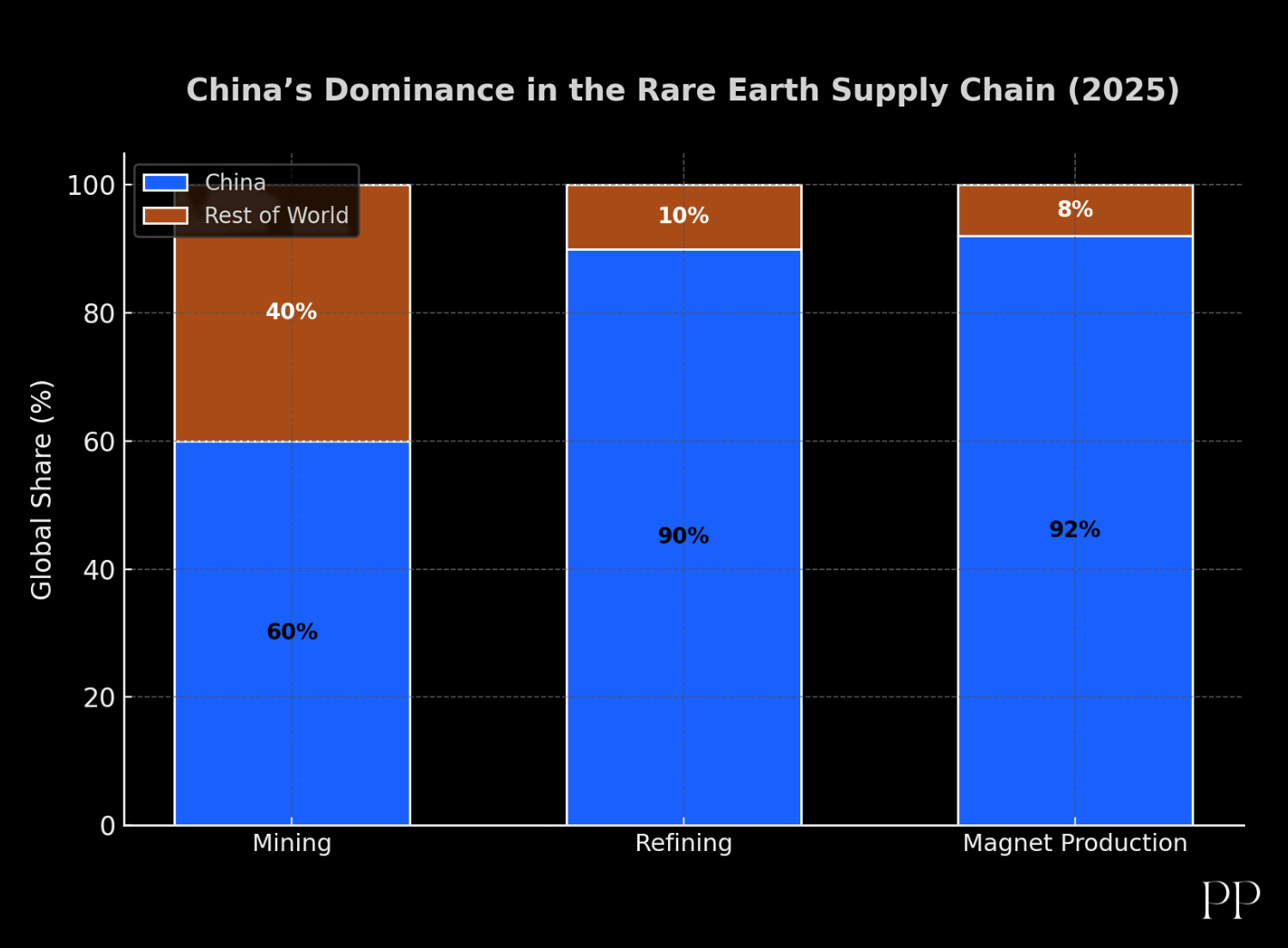

China controls an overwhelming share of global rare-earth supplies. It holds roughly half of the world’s

rare-earth reserves (≈44–50 million tons REO) and accounted for about 69.2% of world rare-earth mine

production in 2024 (≈270,000 tonnes) . The United States is a distant second (≈45,000 t,

~11.5% of

output ). China also dominates processing and downstream production: it refines over 90% of the

world’s rare-earth output and produces about 90% of all high-performance rare-earth magnets . This

vertically integrated supply chain (from mining through refining to magnets) makes China the linchpin of

rare-earth-intensive industries (EV motors, wind turbines, electronics, etc.).

Country

Rare Earth Mine Production (2024)

China

270,000 tonnes

United States

45,000 tonnes

Myanmar

31,000 tonnes

Australia

13,000 tonnes

Nigeria

13,000 tonnes

Thailand

13,000 tonnes

Stage/Category

China’s Share

Rest of World

REE mine production (2024)

~69%

~31%

REE processing/refining capacity

>90%

<10%

High-performance magnet output

~90%

~10%

These figures underscore China’s near-monopoly. For example, state-owned China Northern Rare Earth

Group (Bayan Obo deposit, Inner Mongolia) and China Rare Earth Group (Ganzhou heavy-REE center,

Jiangxi) account for the bulk of China’s production and refining . In short, China is by far the dominant

producer and processor of virtually all rare-earth elements (both light and heavy). ...

Policies Regulating Rare-Earths (2024–2025)

China has instituted sweeping regulations to control rare-earth mining, processing, and exports.

Domestically, the 2024 Rare Earth Management Regulations (effective Oct. 1, 2024) declared all rareearth resources as state-owned and imposed strict environmental and safety requirements on mining

and separation. Only designated firms with official permits may mine or process REEs, and annual

production quotas are tightly controlled. In practice, China’s two giant SOEs (China Rare Earth Group and

China Northern Rare Earth Group) receive virtually all national quotas and in turn allocate output to their

affiliates. The 2025 quota totals were modest (≈270,000 t mined, 254,000 t refined, growth ~+5% from

2024). To enforce these limits, new traceability rules (July 28, 2025) require monthly

production reporting and product-flow tracking via a centralized MIIT database. Violating environmental

or quota rules carries heavy penalties (fines up to 5–10× profits, license revocation).

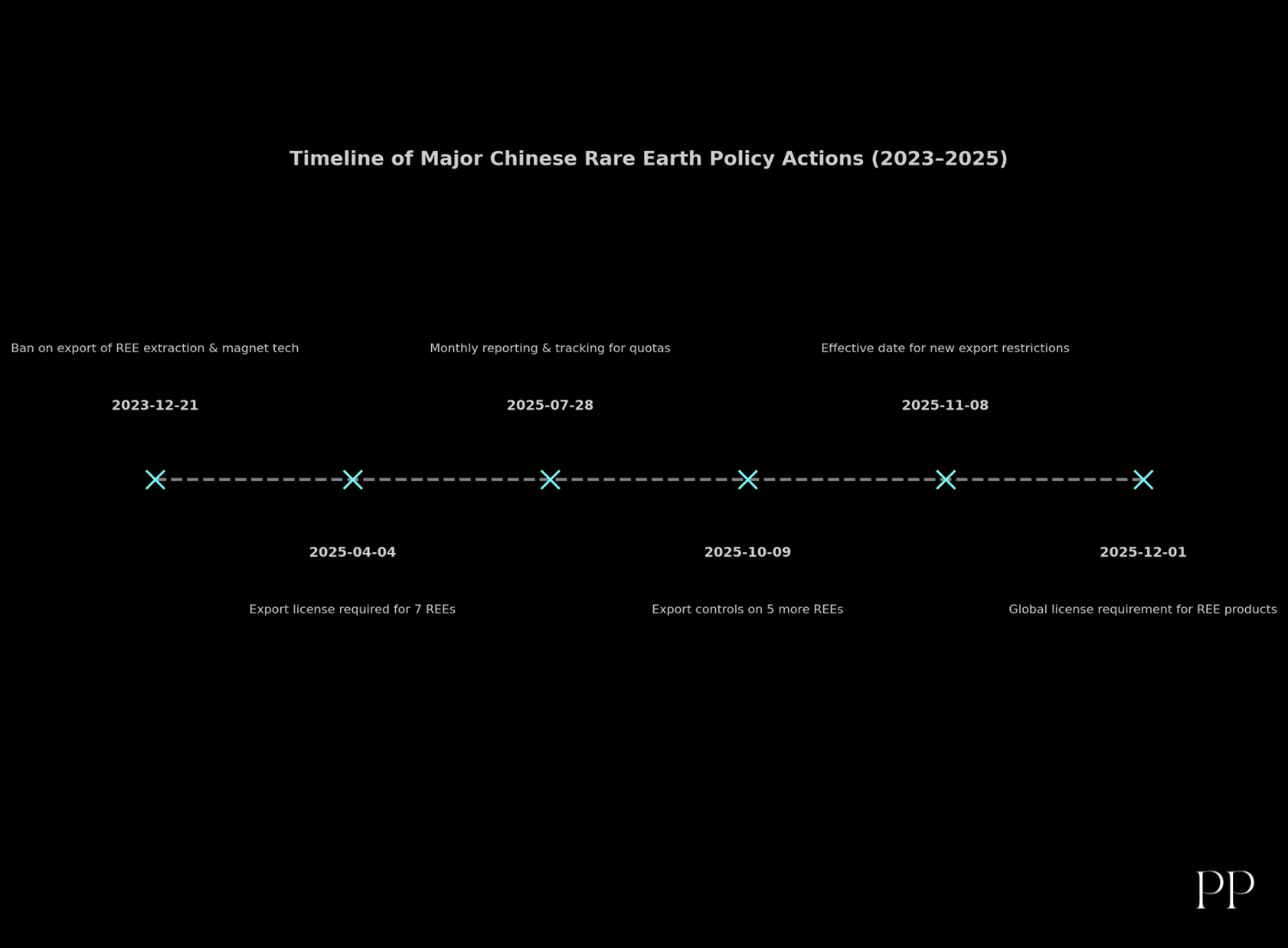

China has concurrently tightened export and technology controls. For example, on December 21, 2023

Beijing banned exports of technology for rare-earth extraction, separation, and magnet manufacturing .

In 2024–25 it imposed new export licensing requirements on various REE materials. On April 4, 2025,

China required export licenses for seven medium/heavy REEs (scandium, yttrium, samarium, gadolinium,

terbium, dysprosium, lutetium) and related compounds . In October 2025 the Commerce Ministry

announced controls on five additional REEs (holmium, erbium, thulium, europium, ytterbium), effective

November 8, 2025 . Most significantly, China introduced a global licensing rule (effective Dec. 1, 2025):

any export of rare-earth magnets or high-tech goods containing even 0.1% of controlled REEs (by origin

or use of Chinese tech) now requires Chinese approval. These measures effectively extend China’s

control extraterritorially, curbing foreign access to rare-earth inputs.

Date

Restriction/Policy

Dec 21, 2023

Ban on export of technology for REE extraction, separation and magnet production

Apr 4, 2025

New export license required for seven REEs (Sc, Y, Sm, Gd, Tb, Dy, Lu)

Jul 28, 2025

Interim measures issued: mandated monthly production reporting and flow tracking for quotas

Oct 9, 2025

Announced export controls on five more REEs (Ho, Er, Tm, Eu, Yb)

Nov 8, 2025

Effective date for the five new REE export restrictions

Dec 1, 2025

Global license requirement for exports of products containing Chinese REEs (≥0.1%)

In short, China’s policies (production quotas, new regulations, export controls) are designed to

consolidate its supply-chain grip and extract strategic leverage in international trade.

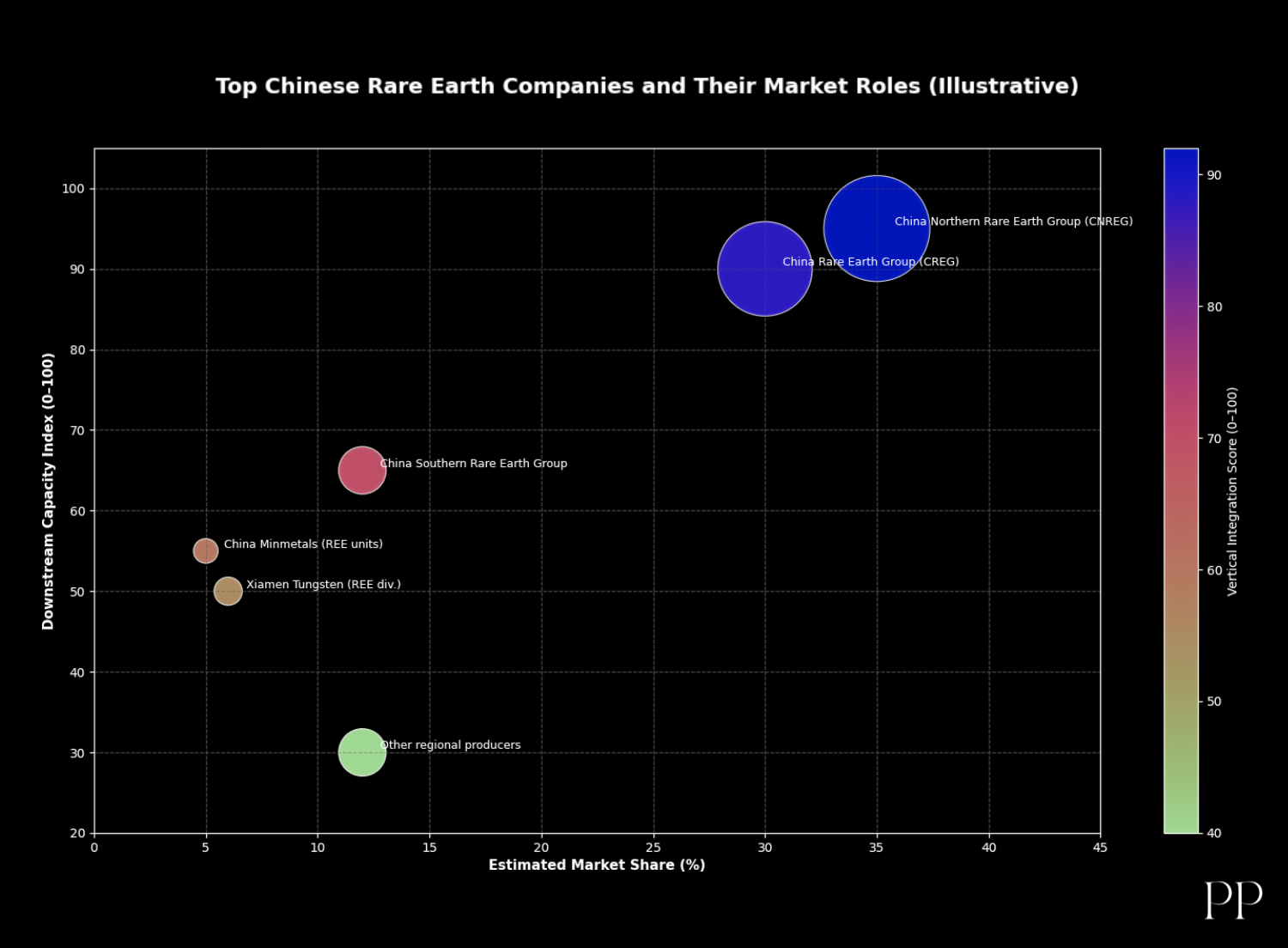

Long-Term Strategies and Industry Control

China’s long-term strategy is to consolidate its rare-earth sector under state control and maintain

technological dominance. Over the past decade the government merged hundreds of firms into a

handful of giants. For example, three state firms were combined into “China Rare Earth Group” in 2021,

which now controls most of China’s heavy-REE supply . Similarly, Xiamen Tungsten Co. (with REE mines

and refineries) is now part of a state-controlled framework. Only a few state-owned enterprise (SOE)

clusters – notably China Northern Rare Earth Group (High-Tech) and China Rare Earth Group – are

eligible for official quotas . This corporate centralization (and a strict “negative list” barring private REE

investment ) ensures the Party can direct investment, R&D, and output. China also invests abroad

(through state funds and BRI partnerships) to secure upstream raw materials, especially from Southeast

Asia and Africa, although detailed 2024–25 data are limited. In all, Beijing’s strategy is one of vertical

integration: dominate the entire REE value chain – from mine to magnet – and leverage that position

geopolitically.

Company

Role/Notes

China Northern Rare Earth Group (High-Tech)

State-owned; world’s largest REE miner, operates the Bayan Obo mines (Inner Mongolia)

China Rare Earth Group Co., Ltd.

State-owned conglomerate (merged from Minmetals, etc.); controls Ganzhou and other mining/refining

China Southern Rare Earth Group

State-owned; major REE producer (ion-adsorption clays in southern China)

Xiamen Tungsten (Rare Earth division)

Once private, now state-affiliated; active in mining/refining, now part of the national REE plan

Economic Impact

China’s rare-earth policies have far-reaching economic effects. Domestically, output controls help

regulate supply to meet national demand while suppressing illegal mining. For example, Beijing has

slowed production growth (2024 quotas up only ~6% vs. +21% in 2023 ) and shut down many small

polluting mines . On the global market, China’s export restrictions and quotas tighten supply, causing

price volatility. When China restricts exports, foreign companies (automakers, electronics, defense firms)

face shortages and cost spikes; e.g. major automakers temporarily cut output when magnet materials

were limited. Conversely, China’s own expansion of production (by increasing quotas) can flood markets

and keep prices low. In fact, analysts note that changes in China’s quotas have an outsized impact on

world prices .

In trade terms, China remains a net importer of raw rare earths (about 129,500 t in 2024) to feed its

vast processing industry , while it is a leading exporter of REE products. In 2024 China exported

~58,142 tonnes of rare-earth magnets (valued ≈US$2.9 billion) . Germany (18.8% of magnet exports) and

the U.S. (12.8%) were the largest buyers. By contrast, China exported only ~17,700 tonnes of raw REE

materials (~US$170 million) in 2024 . This specialization (import ores → export high-value magnets)

illustrates how China monetizes its control of the supply chain. Any Chinese policy change thus

reshuffles the global economy: for example, China’s 2025 export curbs have prompted foreign firms to

seek alternative suppliers and invest in domestic processing capacity (e.g. Lynas in Australia, MP

Materials in the US).

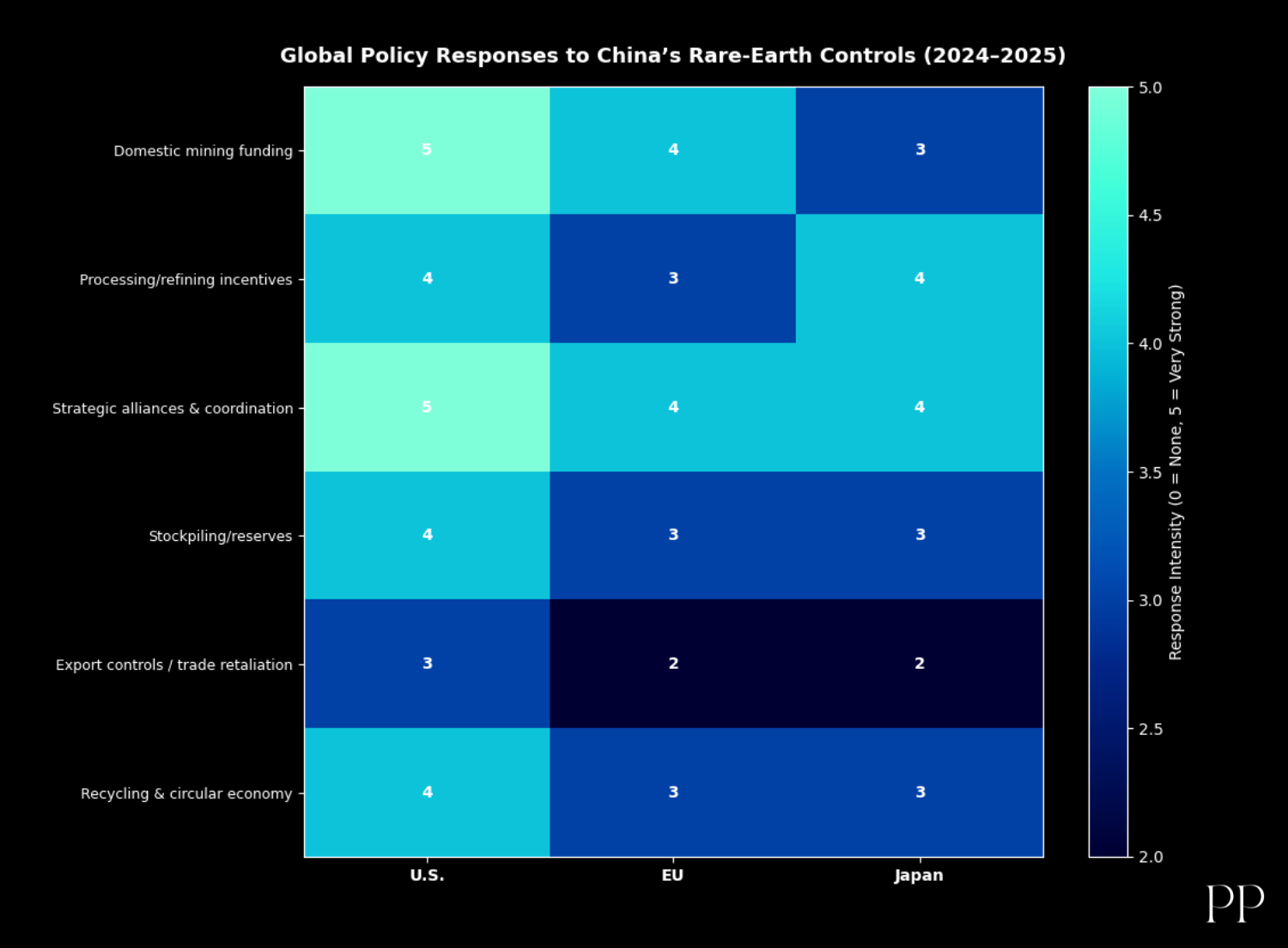

Geopolitical Implications

China’s rare-earth controls have major geopolitical consequences. Western governments see rare earths

as a strategic leverage point. In the U.S., officials warned that China’s export curbs are “China versus

the world” and are pushing allies to diversify supply chains . The U.S. and partners have responded by

funding domestic mining and recycling initiatives and imposing their own export/technology restrictions

(e.g. Biden’s tariffs on REE magnets, and China’s inclusion on the U.S. entity list). President Trump (2025)

has threatened steep retaliatory tariffs on Chinese goods after China tightened rare-earth exports.

In Europe, industry and governments are alarmed. In October 2025 EU leaders debated China’s

“squeeze” on rare earths, as German and Polish officials urged action . Commission President von der

Leyen warned that Europe “cannot afford to fall into new and dangerous dependencies” and announced

plans to secure supply chains . Brussels has convened meetings and even considered triggering its AntiCoercion Instrument to counter China’s moves . Japan has similarly called for a united G7 response, with

its finance minister urging allies to coordinate on China’s export curbs . The knock-on effect is a new

urgency for critical-mineral alliances (e.g. U.S.-led Minerals Security Partnership) as the U.S., EU, Japan

and others seek to reduce reliance on China.

Environmental and Social Considerations

Rare-earth mining and processing carry heavy environmental and health costs, which China’s policies

increasingly acknowledge. Historically, unchecked mining (especially of ionic-clay deposits) left toxic

tailings, acidified waterways, and radioactive waste (thorium/uranium) in some Chinese regions.

Recognizing these hazards, China’s regulations now emphasize strict pollution controls and ecological

protection . For example, the 2024 regulations require enterprises to “implement reasonable

environmental risk prevention [and] pollution prevention” measures . Companies in the rare-earth sector

must comply with laws on clean production, energy efficiency and waste treatment, and violations incur

severe penalties . In recent years Beijing has shut many illegal or high-emission mines as it “cleaned up

its act”

.

Despite stronger rules, environmental challenges remain. The processing of one ton of rare-earth ore

can produce hundreds of tons of toxic waste and radioactive residue. Chinese oversight aims to manage

these risks, but enforcement is uneven. The new traceability and inspection regimes (e.g. monthly

reporting, audit powers) are intended in part to prevent companies from evading environmental

standards . In summary, environmental concerns have become integral to China’s rare-earth strategy:

resource protection and pollution control are now official policy goals alongside industrial and security

objectives.

Sources: Recent data and analyses from industry and government reports (USGS, IEA) and expert commentary . This report draws on

up-to-date publications (2024–2025) to detail China’s rare-earth policies, market data, and their global impact.