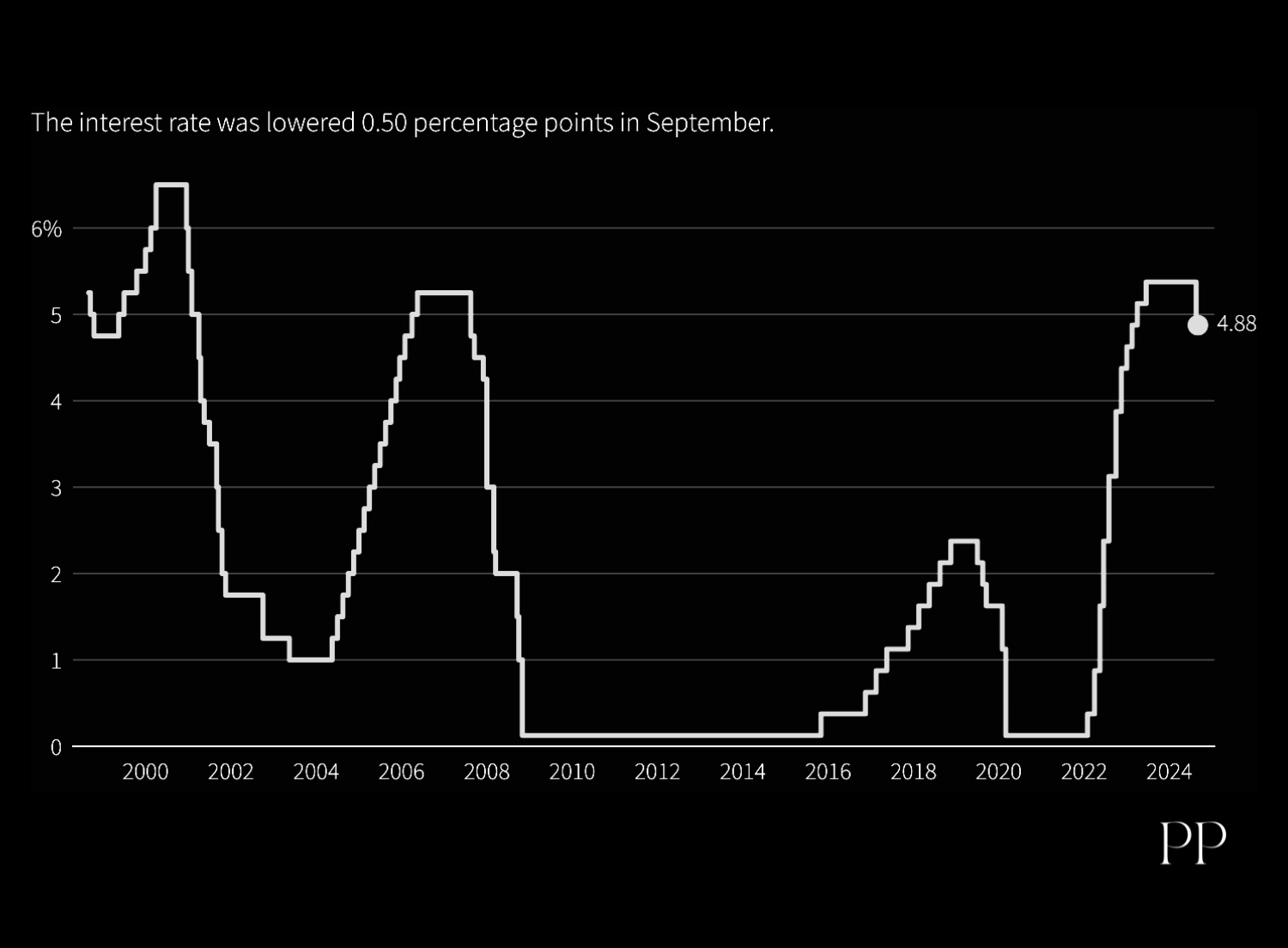

On Sept. 17, 2025 the Fed’s FOMC cut its benchmark rate by 25 basis points – the

first cut of the year – lowering the federal funds target range from 4.25–4.50% to 4.00–4.25%.

This quarter-point reduction was widely expected by markets and brings the benchmark rate to

its lowest level in 10 months.

Why the cut

Fed officials emphasized a weakening labor market as the key driver. Recent data

showed job gains slowing and the unemployment rate edging up (to 4.3% in August, a 4‑year

high). Inflation remained above the Fed’s 2% goal and may rise further (tariffs are feeding prices)

, but the “downside risks to employment have risen,

” the Fed noted. In other words,

policymakers judged that supporting jobs outweighs fighting still-elevated inflation. As Chair

Jerome Powell put it, this “risk management” cut is preventative, to guard against growing

uncertainty.

Outlook

The Fed opened the door to further easing. Policymakers’ projections (the “dot plot”)

signal additional cuts this year (two 25‑bp cuts penciled in) and into 2026 . Markets broadly

expect a gradual easing cycle, though forecasts vary widely among economists. ...

Fed Rate Cut Over Years

Source: The Both Chart Are By Reuters and Their Credit and Right Goes to Reuters.

Decision Drivers & Context

The September cut reflects a shift from the Fed’s earlier hawkish stance. Since late 2024, the Fed

held rates at 4.25–4.50% amid persistent inflation. But by mid-2025 economic growth had

moderated: GDP was running roughly 1–2% (Fed projects ~1.6% for 2025 ), consumer spending

and business investment were slowing, and “recent indicators suggest growth of economic

activity moderated”

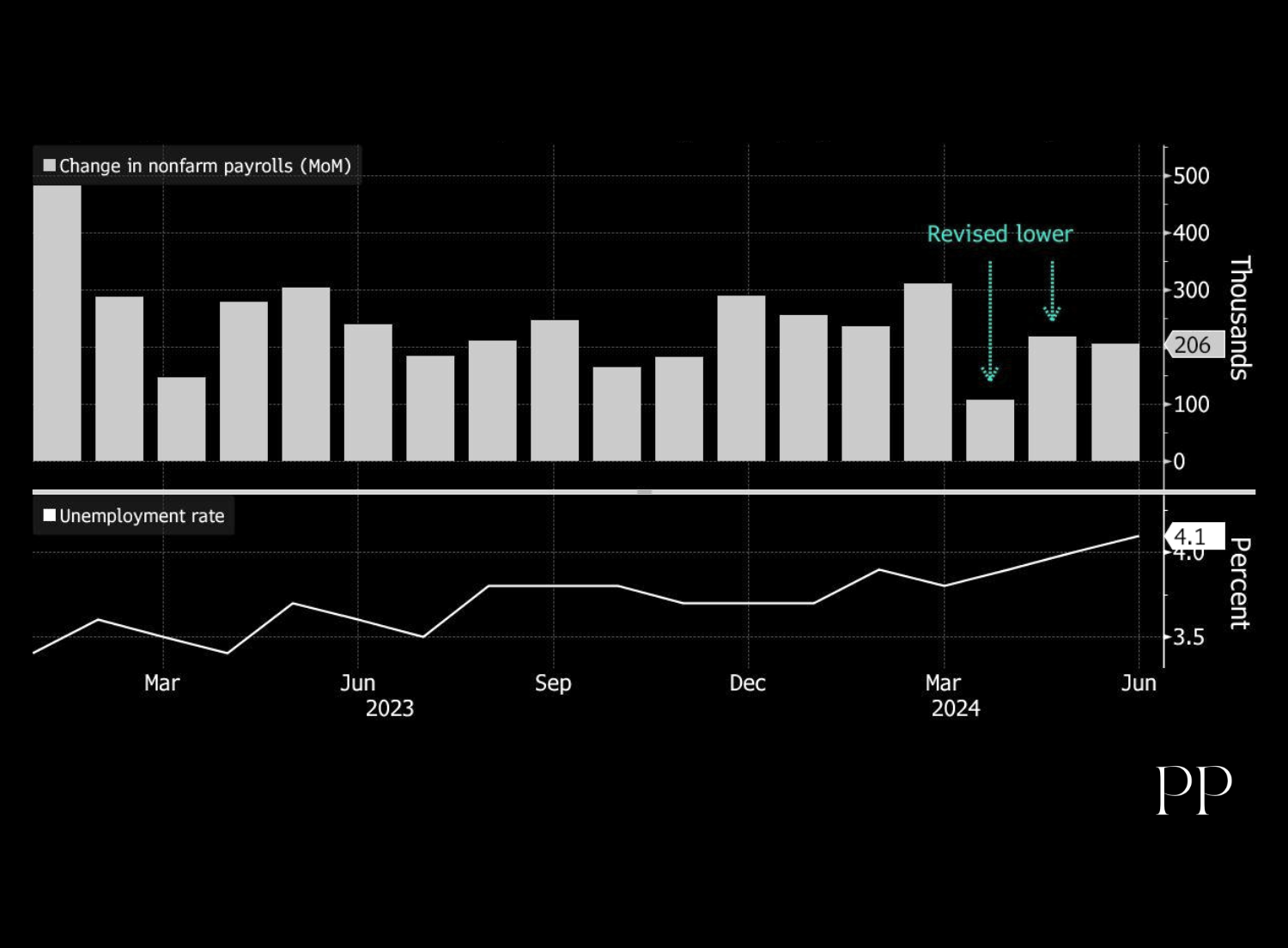

. Notably, job growth has cooled significantly. One high-profile factor was

labor revisions: mid‑2025 payroll data were revised down by nearly 900,000 jobs , consistent with

reduced worker demand. Immigration flows also slowed, tightening labor supply.

Figure: U.S. nonfarm payroll gains (bars) and unemployment rate (line) through August 2025. Payrolls additions have dwindled and

unemployment has risen to 4.3% , illustrating the cooling labor market cited by the Fed.

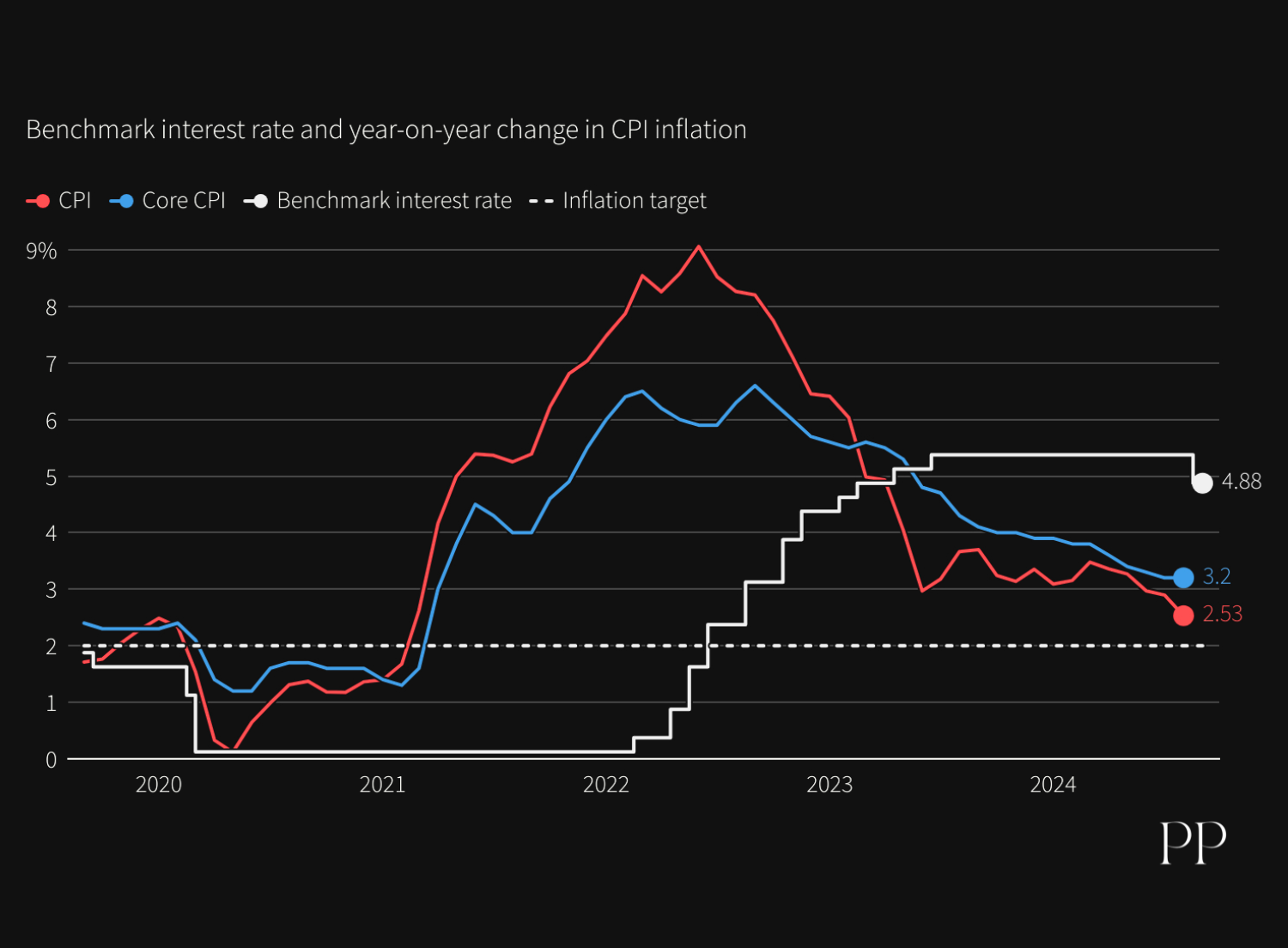

Inflation remains elevated: core PCE inflation is around 3.0–3.2%. Recent increases have been

driven by goods price jumps due to tariffs . The Fed acknowledged these are largely one-time

level shifts, but it cannot ignore them . Thus the policy decision involved balancing the Fed’s dual

mandate. In Fed statements and Powell’s press conference, officials noted that “job gains have

slowed” and downside risks to employment had risen, even though inflation is above target.

Many analysts interpret this as the Fed prioritizing job support given the labor data.

Economists describe the move as a compromise: some Fed officials (like newly confirmed

Governor Stephen Miran) pressed for a larger cut (50 bps) , while others feared adding

inflationary pressure. The 25-bp cut “likely reflected a compromise” between those more

concerned about inflation and those worried about unemployment.

Implications & Outlook

By signaling rate cuts, the Fed has shifted toward an easing bias. The FOMC’s dot plot now shows

the median federal funds rate falling to around 3.6% by end-2025 . Policymakers expect inflation

to drift down modestly (PCE ~3.0% in 2025) and unemployment to rise to about 4.5% next year .

Thus, the Fed is bracing for slower growth and a softer labor market ahead. In its statement the

Fed emphasized it “will continue to monitor incoming data” and stands ready to adjust policy as

needed.

Analysts note that the Fed’s cut is intended to “get ahead of a slowdown without overreacting”

,

rather than signal panic . The broad expectation is for a gradual easing cycle. For example,

Fidelity forecasts that “more rate cuts are likely to follow” pending how jobs and inflation

evolve . However, with inflation still high, the Fed indicated it won’t hit its 2% target until 2028,

so future moves will be data‑dependent.

Sector Impacts

Housing market

Mortgage rates have already eased in anticipation. The 30-year fixed rate has

fallen from last summer’s 7–8% down to about 6.3–6.4%, the lowest in roughly a year. As a result,

borrowing costs for buyers are inching lower. Homebuilders benefit directly: lower rates cut the

cost of construction financing (especially acquisition/land development loans), which should help

ease housing supply constraints. However, builders caution that many structural issues (high land

and labor costs, zoning constraints) persist and can’t be solved by rates alone . In the near term,

economists expect some improvement in affordability: many homeowners are refinancing, and

home prices may stabilize if demand picks up. But NAHB notes the housing market overall

remains weak, and chief economists say any pickup will be gradual.

Stock market

Lower rates are generally positive for equities (cheaper money boosts

valuations). Indeed, broad equity indexes held near record highs. On announcement day the Dow

Jones Industrial Average rose about 0.6% while the S&P 500 and Nasdaq slipped modestly. A

Reuters market wrap noted that “world stocks hit a record high” even as U.S. large-caps ended

mixed. Global equity markets were mostly flat to slightly up. Some strategists observed a mild

“sell-on-the-news” reaction – markets had rallied on the expectation of a cut, so traders took

profits once it was delivered. Bond yields climbed slightly (10-year U.S. Treasury +0.05 point),

tempering gains. Still, many analysts say an easing Fed should support stocks: lower discount

rates favor growth sectors. For example, BlackRock strategists note that Fed cuts make growth

stocks (especially tech) more attractive and that the dollar is likely to weaken, which can benefit

international stocks. Overall, investor sentiment remains cautiously optimistic: equity valuations

are high but supported by the Fed’s easing path.

Consumer loans

The Fed cut mainly lowers short‑term rates. Its first effect is on variable‑rate

loans and credit products tied to the prime rate. Credit card and adjustable-rate borrowers

should see slightly lower payments over time. WalletHub estimates Americans with credit cards

could save roughly $1.9 billion in interest costs next year due to the cut. Home equity lines

(HELOCs) — which are directly priced off the Fed funds rate — should drop by about 0.25%. For a

$100,000 HELOC, CBS calculates this means roughly $170–$180 per year in savings. By contrast,

fixed-rate loans (like most mortgages and student loans) do not change immediately; those

borrowers would benefit only if they refinance. On the flip side, savers’ rates will tick down: banks

are beginning to reduce yields on high-yield savings accounts and CDs, which were around 4–5%

in 2024.

Expert Opinions and Forecasts

Analysts and policymakers widely described the cut as prudent given the data mix. Fed Chair

Powell framed it as a “risk management” action to address downside risks to the economy . At

the meeting, one Fed governor (Miran) dissented, arguing a 50‑basis-point cut was justified .

Economists note the Fed’s projections now imply about two more cuts in 2025: the median dotplot shows rates ending 2025 near 3.6% (about 75–100 bps below current levels) . Forecasters

project inflation around 3.0% next year and core inflation ~3.1% , with unemployment rising

toward 4.5–4.6%. Oxford Economics’ Michael Pearce points out that Governor Miran’s aggressive

outlook (a total 125 bps cut this year) is an outlier and pulled down the median projection .

Several strategists responded positively. Seema Shah (Principal AM) said the Fed’s dot-plot of two

more cuts “reinforces the notion that today is the first in a sequence of cuts” and “should give

markets a positive boost”

. Bill Adams (Comerica Bank) noted the split in Fed views – 10 officials

see at least 50 bps of easing vs. 9 seeing ≤25 bps – reflecting caution in the outlook. Matt Schulz

(LendingTree) commented that “any reduction is welcome” for consumers, even if modest.

Conversely, some like Goldman Sachs’ Mark Malek warned the market may stay volatile: he

expected a “negative knee‑jerk” after the initial rally, given how much optimism was already

priced in.

Market Reactions (Sept. 17, 2025)

On announcement day, U.S. markets showed only moderate moves: the Dow rose ~0.57% while

the S&P 500 and Nasdaq slipped ~0.10–0.30% . European stocks were essentially flat. Treasury

yields actually rose slightly (the 10-year yield +4.6 basis points to ~4.07% ), as Powell’s remarks

eased fears of an aggressive easing. The dollar strengthened modestly (e.g. trade-weighted dollar

+0.35% ). Gold briefly hit a new high above $3,700/oz, then settled down around $3,660 . Oil

prices fell (Brent and WTI down ~0.7%), as weaker demand signals outweighed any inflation

impact.

Investor sentiment was mixed. Reuters noted “world stocks hit a record high” even as U.S.

indices barely budged. Many commentators described a “sell-the-news” tone – markets had

rallied on Fed-cut hopes, so traders took profits on the news. Still, as Seema Shah remarked, the

Fed’s message was broadly “measured”

, easing just enough to address early signs of strain

without overreacting.

Sources: Federal Reserve (FOMC statement); Fed officials’ press conference; market and finance news reports; analyses by Fidelity,

NAHB, Fox Business, CBS News, Bankrate , and others as cited. The information is current as of September 2025.