Over the past year Oracle has posted record AI‑driven growth, especially in cloud and enterprise

software, but it remains a smaller player compared to hyperscale rivals. In Q1 FY2026 (ended Sep.

2025), Oracle’s cloud revenues (IaaS+SaaS) rose 28% YoY to $7.2 B and its infrastructure (OCI)

grew 55% to $3.3 B . Crucially, Oracle’s remaining performance obligations (future bookings)

jumped to $455 B (up 359% YoY) – a sign of strong demand. Much of this growth is attributed to

AI: Oracle reported “multi-cloud database” revenue (Oracle Database running on AWS/Azure/GCP)

up 1,529% , and it bundles leading LLMs (ChatGPT, Gemini, Grok, Llama) into its platform to let

enterprises run AI on their data.

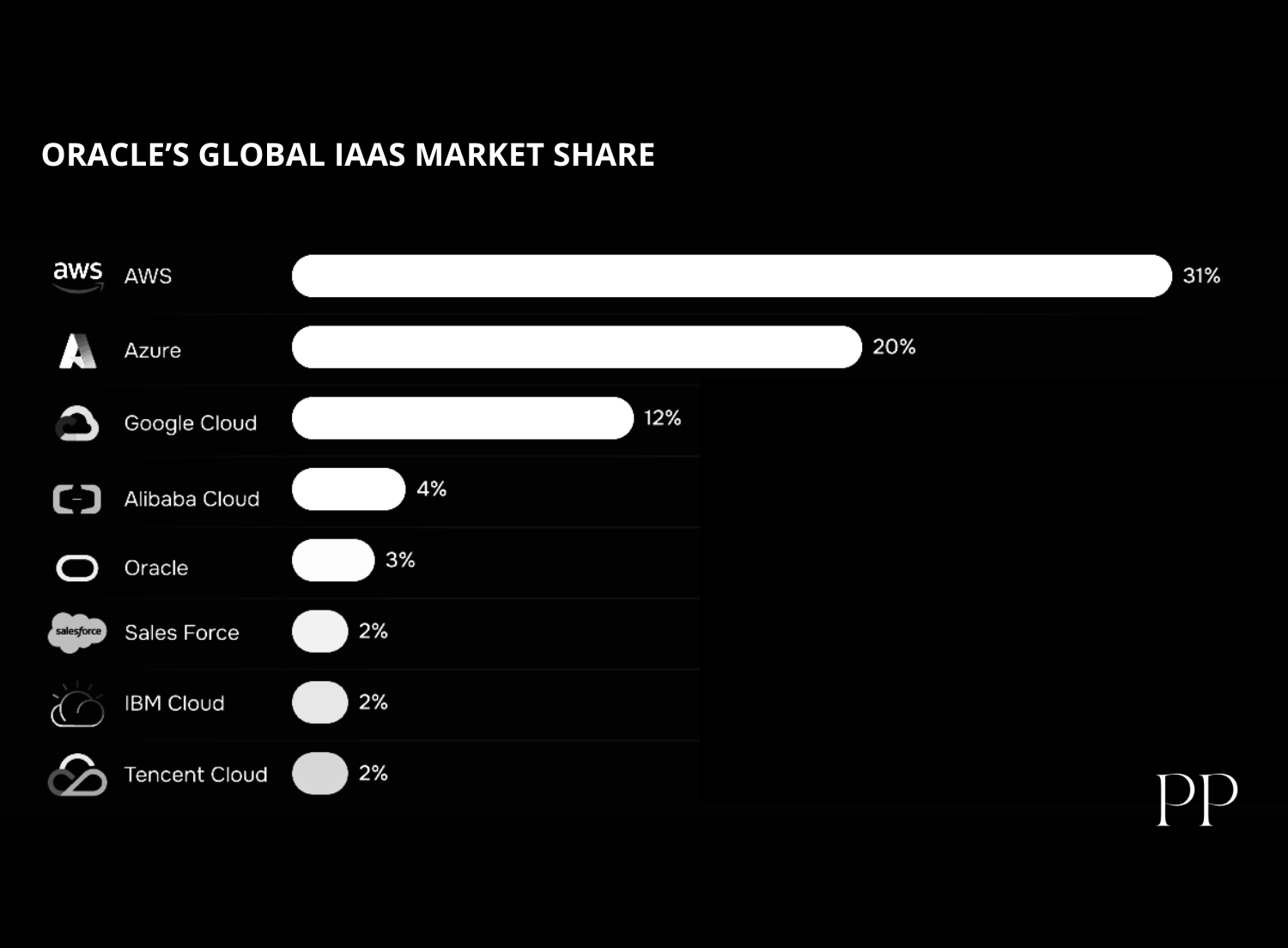

However, Oracle’s share of the overall cloud/AI market is still small. Synergy data show Oracle

held only about 3% of global IaaS market share in Q1 2025 , far below Amazon (29%), Microsoft

(22%) and Google (12%). Competitors remain much larger: for example, AWS revenue grew 17.5%

in Q2 2025 (to $30.9B) and Google Cloud grew 32% , while Microsoft Azure (as part of

Azure+cloud services) grew ~39% (surpassing $75B annual run-rate ). In enterprise software,

Oracle’s Fusion Cloud suite now includes dozens of new GenAI features (e.g. 50+ GenAI tools

announced at CloudWorld 2024) and achieved strong growth (Fusion ERP +17%, NetSuite +16%

YoY in Q1) . Its overall 2024 revenue ($53.8B) still exceeds pure‑play SaaS rivals like Salesforce

(~$34.9B) or SAP (~$33.3B) . In healthcare, Oracle (via its Cerner acquisition) is pushing an

“AI‑first” EHR on OCI , but Epic remains dominant (42.3% share vs Oracle’s 22.9% in hospital

EHRs ). In sum, Oracle is growing fast with AI – especially in enterprise workloads – but its

absolute scale and market share trail the cloud giants.

Cloud Infrastructure and AI Services

Oracle’s Cloud Infrastructure (OCI) is the centerpiece of its AI strategy. In the past year Oracle

launched a range of AI‑focused services on OCI: for example, OCI Generative AI Agents (a

managed RAG service using vector search on Oracle’s 23ai database) and support for large

models like Meta’s Llama 3 . Oracle also announced an upcoming AI Database service that lets

customers run LLMs directly over their enterprise data . CEO Larry Ellison has emphasized OCI’s

technical advantages – notably, very fast GPU‑network connectivity and optimized storage – which

he claims make Oracle’s inference workloads twice as fast (and half as costly) as rivals . These

design choices position Oracle as focusing on high-performance inference (running AI models on

data) rather than on the massive model‑training market.

This strategy is driving rapid growth. In Q1 FY2026, OCI revenue was $3.3B (up 54% YoY) , and

OCI consumption (usage) grew 57% . Oracle’s multi‑year forecast shows OCI growing 77% in

FY2026 (to $18B) and then accelerating in subsequent years . Meanwhile, many large enterprises

are signing multi‑billion‑dollar cloud contracts: Oracle signed four deals in Q1 totaling billions,

pushing its RPO backlog to $455B (nearly half a trillion in committed future revenue). Oracle

reports that demand for GPU cloud is outstripping supply, and that large customers (including AI

labs) are rapidly moving Oracle racks into AWS, Azure and GCP regions. ... Despite this momentum, Oracle’s global IaaS market share is still single‑digit. Synergy Research data for Q1

2025 show:

This small share highlights the scale gap: AWS, Azure and Google lead the market. (Oracle’s share

is flat to up – it was ~2% a year earlier – but remains far behind.) However, Oracle’s share is

growing from a low base: it is winning large enterprise deals (particularly for dedicated

“cloud@customer” racks) and benefits from embedding its tech on other clouds. For example, Q1

FY2026 multi‑cloud database revenue (Oracle DB on AWS/Azure/GCP) surged 1,529% YoY , as

Oracle delivers co‑located regions in multiple hyperscalers.

By comparison, the cloud leaders are also investing heavily in AI: AWS re:Invent 2024 emphasized

new Bedrock models and AI accelerators, Google Cloud rapidly expanded its TPU‑based

infrastructure and Vertex AI platform, and Microsoft Azure became “AI‑first” in every region with

massive new datacenter capacity . In the latest results: Azure (via Microsoft Intelligent Cloud)

grew ~39% , Google Cloud grew 32% , and AWS grew ~17.5% . Overall cloud spend is

skyrocketing (Synergy: +23% total cloud IaaS YoY ), led by 140–180% growth in AI‑specific services.

Market Adoption: Oracle cites dozens of new customers and some multi‑$B contracts. By RPO

(contract backlog) it claims unmatched visibility into future demand (up 359% YoY) . Its customers

range from financial services to manufacturing to consumer goods, seeking to run AI on their

private data. However, major public cloud customers still mostly use AWS/Azure; Oracle is often

adding Oracle services in addition (e.g. running Oracle DB on AWS) rather than replacing them. In

short, Oracle’s cloud is the fastest-growing but still niche: it wins on performance/cost for AI

inference in enterprise settings, but AWS/Azure/Google dominate overall cloud usage.

Enterprise Software (SaaS/ERP/CRM)

Oracle’s traditional strength is enterprise applications (ERP, HCM, CRM, supply chain, CX). In the

past year it has deeply infused these apps with AI. For example, Oracle rolled out ~50 new GenAI

features in its Fusion Cloud Applications suite , covering finance, HR, customer service, supply

chain and sales. These include tools like AI‑assisted invoice reconciliation, auto‑generated

knowledge articles for support agents, sales‑copilot emails, and more. Oracle also launched an

Oracle AI Agent Studio that lets customers build custom AI “agents” embedded in workflows . In

the database layer, Oracle’s Fusion Data Intelligence Platform now supports AI/ML on any data

(including third‑party sources) and offers a vector database so LLMs can query transactional data

securely.

Oracle’s enterprise cloud revenue is growing steadily. In Q1 FY2026, SaaS (applications) revenue

was $3.8 B, up 11% YoY . In particular, Oracle Fusion ERP cloud hit $1.0 B in the quarter (up 17%)

and NetSuite cloud ERP also $1.0 B (+16%) . These double‑digit growth rates indicate solid market

adoption, though the base is far smaller than older on‑premise deployments. Importantly,

Oracle’s strategy is database‑centric: it enables customers to keep all data in Oracle Database and

simply point generative AI models (their choice of LLM) at it, rather than moving data out. This

creates an “enterprise moat” by addressing data security and governance for AI.

By contrast, key competitors are also pushing generative AI but with different approaches.

Salesforce (leading CRM) unveiled its Einstein 1 platform (Copilot in every app) , while SAP

announced its “Joule” AI assistant to permeate S/4HANA Cloud and SuccessFactors . Microsoft has

embedded Copilot across Microsoft 365 and Power Platform, and is adding AI to Dynamics 365

(its ERP/CRM suite) via Azure AI. (For example, Microsoft reported Dynamics 365 revenue up 23%

in FY2025 .) All of these platforms aim to automate tasks (predictive analytics, content generation,

workflow automation) within enterprise applications.

As one measure of scale, consider 2024 revenues of these vendors: Oracle as a whole was

~$53.8 B (mostly licenses, SaaS and cloud infrastructure), while Salesforce was ~$34.9 B and SAP

~$33.3 B . This reflects Oracle’s broader product portfolio (databases and middleware as well as

apps). Even so, analyst reports note that Oracle’s perceived AI advantage (via Oracle CloudWorld

hype) has not yet translated to large market share gains – its SaaS footprint is still well below

market leaders in each app category.

Vendor

Latest Annual Revenue

Oracle

$53.8 B (FY2024)

Salesforce

$34.9 B (FY2024)

SAP

$33.3 B (FY2023)

Table: Major enterprise software vendors (2023/24 revenues) . Oracle’s total is larger than any single SaaS

specialist.

Technical innovation: Oracle’s key innovation claims are around architecture and integration. It

argues that by co‑designing database, middleware and cloud, it can add AI with lower risk. For

example, Oracle’s Autonomous Database has added GenAI capabilities so that customer data

can be queried by LLMs without export . Its OCI GenAI and agent services are tightly integrated

with Oracle DB and applications (via the Fusion Data Intelligence Platform) . In comparison,

Microsoft and Google have focused on building general AI platforms: Microsoft’s Azure OpenAI

Service and Power Platform Copilots, Google’s Vertex AI and Gemini-based apps. Oracle’s

“narrow AI” approach (directly in ERP/finance tasks) may yield quicker enterprise wins, but is less

flexible than the open ecosystem of AWS/GCP.

Healthcare AI

Healthcare is a critical vertical where Oracle is investing heavily via its Cerner acquisition. In 2025

Oracle re‑branded Cerner as “Oracle Health” and launched an all‑new AI‑powered EHR platform

on OCI . This next‑gen EHR (for ambulatory care, with inpatient support coming in 2026) was built

with multimodal AI: it features a voice‑driven interface and an embedded “Clinical AI Agent” that

can summarize medical records and suggest care recommendations . Oracle also offers AI tools

for providers and patients – e.g. a voice‑enabled Oracle Clinical Digital Assistant for clinicians and

a GenAI patient assistant for handling records . These aim to reduce documentation burden and

improve access to insights in Cerner data.

Despite this push, Oracle’s market adoption in U.S. healthcare remains modest. In acute hospital

EHRs, Epic Systems is still dominant. According to KLAS data, Epic had a 42.3% share of the U.S.

hospital market in 2024, while Oracle (Cerner) held 22.9% . (Oracle’s share actually declined

slightly over the year.) Oracle lost a net 74 hospitals in 2024, whereas Epic continued to gain.

Thus, while Oracle’s new EHR may help stem this loss, it will take time to regain share from

incumbents.

EHR Vendor

U.S. Hospital EHR Market Share (2024)

Epic Systems

42.3%

Oracle (Cerner)

22.9%

Table: Epic vs. Oracle (Cerner) share of U.S. acute care EHR market .

Other tech giants are also racing in healthcare AI. For example, Microsoft has long integrated AI

into its health offerings – notably by embedding Azure OpenAI into Epic’s platform under a 2023

partnership – and offers cloud services like Azure Health Data Services. Google Cloud promotes AI

for genomics and imaging (e.g. Google Health and DeepMind projects) and has specialized

healthcare tools (BigQuery for Health, Vertex AI). AWS similarly markets GenAI tools (via Bedrock)

to healthcare (e.g. HealthLake). None of these cloud platforms report separate healthcare

revenue, but all target life sciences and hospitals with AIoptimized infrastructure. Oracle’s focus

on healthcare is distinctive because it owns an EHR product, but it competes against Epic’s heavy

customer base and the AI initiatives of the big clouds.

Conclusion

Oracle has clearly accelerated in the AI race across its core sectors. Its cloud and database

growth are exceptionally strong, driven by enterprise AI demand, and it has boldly retooled its

software (ERP, HCM, CRM, healthcare) to embed generative AI. Technically, Oracle touts

advantages in network performance and data integration that can make AI inference faster and

more secure. In financial metrics, Oracle reported one of its best quarters ever (thanks to AI

cloud demand).

However, in absolute terms Oracle is not “winning” the AI race over AWS, Microsoft, and Google

– those vendors remain far larger in cloud infrastructure and have massive footprints. Oracle’s

IaaS market share is still only ~3% , versus 29% for AWS, 22% for Microsoft and 12% for Google .

Its cloud base is growing rapidly (often on AI workloads), but from a much smaller base. In

enterprise apps, Oracle keeps pace with AI features but competes against equally aggressive

moves by Salesforce, SAP and Microsoft. In healthcare, Oracle is innovating (voice‑AI EHR) but

Epic continues to lead in adoption.

Overall, Oracle is a rising competitor thanks to its AI innovations and strong enterprise

base, but it has not overtaken the market leaders. It excels in embedding AI into existing

enterprise databases and applications (creating a “private data + LLM” approach), which gives it a

niche advantage for secure enterprise AI. Yet scale still favors AWS/Azure/Google, which are

winning most large cloud and AI contracts. Oracle’s strategy seems to be “compete on

performance and integration,” which could yield long‑term gains – but in the last 12 months,

Oracle is a fast‑growing contender rather than the undisputed winner of the AI race.

Sources: Oracle press releases and financial reports ; industry analysis and news (VentureBeat , CRN , FierceHealthcare , TechTarget ,

Futurum , FinancialContent/WRAL , Microsoft earnings , etc.). These cover developments through mid-2025.