Many indicators echo past tech manias. Stocks of leading AI firms have

soared to record highs disconnected from earnings, and venture funding is unprecedented (e.g.

in 2025 Silicon Valley raised $111B, with 93% into AI start-ups) . Academic tests detect “explosive”

price patterns in tech indices . High-profile commentators warn that today’s P/E ratios exceed

even the late-1990s dot-com levels , and fabled dot-com bubbles are frequently invoked as

analogies.

Contrarian Viewpoints

Other experts argue the AI surge is driven by genuine innovation. AI

infrastructure build-out and productivity gains could justify higher valuations in time . Unlike

many bankrupt dot-coms, current AI leaders (Nvidia, Microsoft, Google) are profitable businesses

expanding into new markets. Some prominent investors (e.g. Jordi Visser) believe the AI

revolution will “drive all investment gains” and caution against “fading” AI.

Media & Hype

Coverage has oscillated between euphoria and skepticism. Tech leaders issue

hyperbolic claims (calling AI “more profound than fire” ), and headlines trumpet trillions in

opportunity . Simultaneously, analysts flag disappointing early ROI: Gartner predicts ~30% of AI

pilots will be abandoned , and one survey found ~95% of companies see no benefit from

generative AI so far.

Historical Parallels

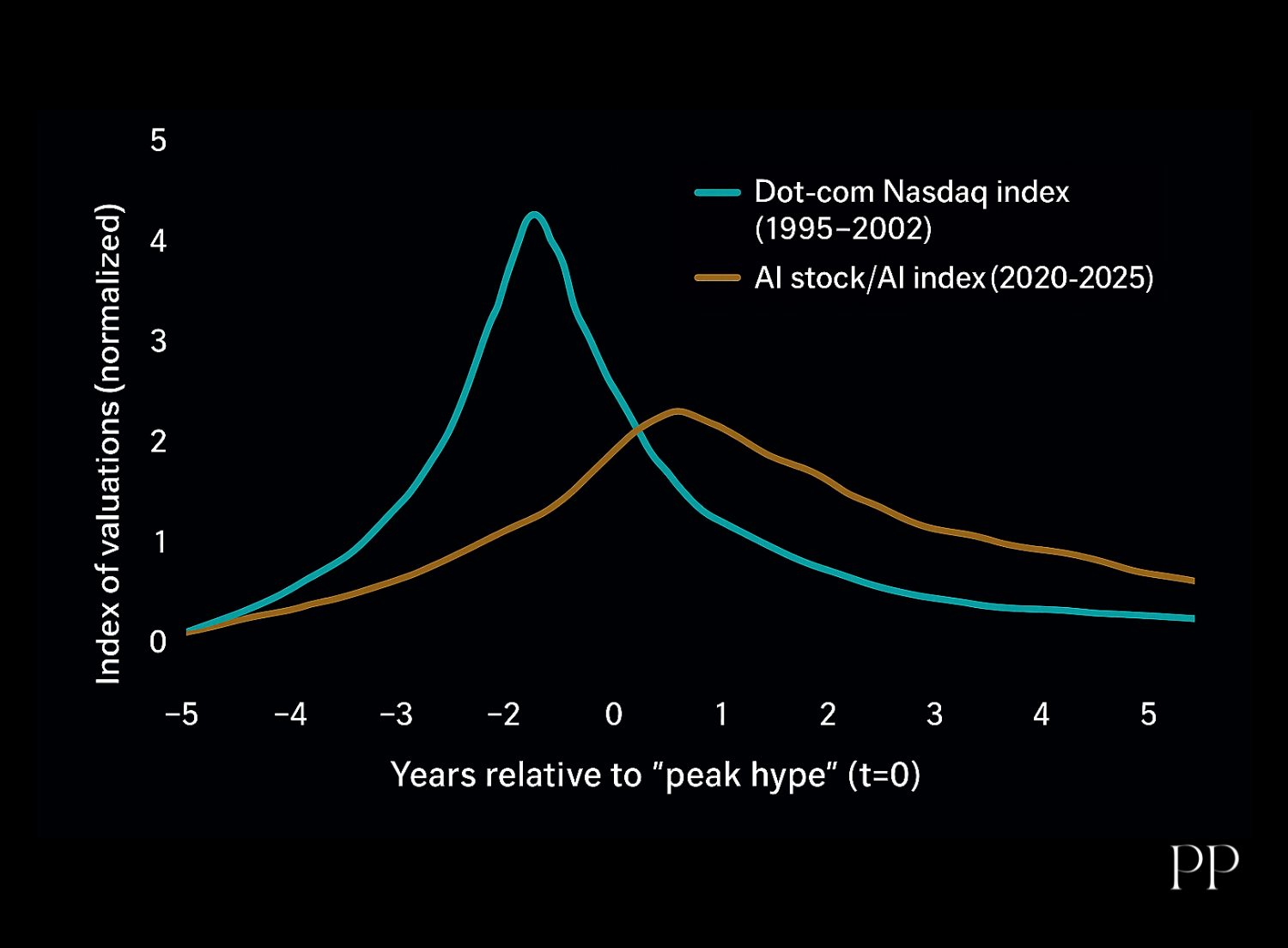

The late-1990s dot-com bubble provides a sobering backdrop. From 1995–

2000 the Nasdaq quintupled, then crashed ~78% by 2002 . In that boom, investors chased “story

stocks” with scant profits . Similar dynamics—heated storytelling (“AI will be bigger than the

Internet”) and speculative funding—are evident today. However, the scale of today’s AI

infrastructure and the productive use cases under development may ultimately yield lasting

growth beyond what dot-coms produced.

In Sum

evidence is mixed. Many objective measures—soaring valuations, frenzied investment, skyhigh

P/Es—match textbook bubble patterns . Yet others caution that AI’s transformative potential could

sustain high investment. Observers advise vigilance: as Altman himself admits,

“investors as a whole are

overexcited about AI”

, suggesting the situation bears close watching.

Historical and Academic Perspectives on Bubbles

A “speculative bubble” is traditionally viewed as a self-reinforcing rise in asset prices that decouples

from fundamentals . Shiller describes it as a “social epidemic”: media-driven stories amplify price gains,

which in turn fuel more buying, until the eventual bust . Academic analyses of technology bubbles note

this cyclic pattern: initial innovation leads to excitement and investment, which overshoots real

productivity and then reverses.

Valuation Comparison (AI vs Dot-Com)

Dot-Com Bubble (1995–2000)

The most cited tech bubble. The Nasdaq Composite (heavy in

internet stocks) surged ~600% from 1995 to March 2000, then plummeted ~78% by late 2002 . At

the peak, unprofitable web companies had fantastical valuations—“story stocks” that ignored

profits . When interest rates rose and earnings failed to appear, the bubble popped, wiping out

trillions in market value. Alan Greenspan’s famous “irrational exuberance” speech captured the

ethos of that era.

Other Bubbles

Scholars compare AI fears to other episodes. For example, borrowing a line

from a dot-com boom hedge fund, one analyst said today’s AI investment frenzy is like “Global

Crossing reborn” (referring to 1999’s overbuilt telecom fiber networks) . Some even liken it to the

pre-2007 housing boom . The key lesson: unchecked hype can yield ruin (e.g. Tulip Mania, 1929

crash).

Other Bubbles

Scholars compare AI fears to other episodes. For example, borrowing a line

from a dot-com boom hedge fund, one analyst said today’s AI investment frenzy is like “Global

Crossing reborn” (referring to 1999’s overbuilt telecom fiber networks) . Some even liken it to the

pre-2007 housing boom . The key lesson: unchecked hype can yield ruin (e.g. Tulip Mania, 1929

crash).

Economic Frameworks

While definitions vary, many economists stress the role of expectations

and narratives. a bubble as rapid price runs, disconnected from fundamentals, driven by

captivating narratives . Importantly, they note it’s hard to identify a bubble in real time —usually

only obvious in hindsight. This frames the AI question: have fundamentals caught up with

valuations (a boom), or is it a self-propelled mania (a bubble)? ...

AI Market Valuations and Investment Trends

Figure: Nvidia’s market value exploded in the AI era. Reuters/LSEG data shows Nvidia’s cap roughly ~1500% higher in

2025 than in 2020 (left scale), far outstripping its tech peers. (Chart by Reuters).

Nvidia’s ascent illustrates the fervor. By July 2025 Nvidia briefly became the world’s first \ $4 trillion

company . (For context, it was under \$1 trillion as recently as mid-2023 .) Its stock is up ~700% since late

2022 , as data-center demand for AI chips booms.

Venture Capital

AI start-ups are drowning in capital. In Silicon Valley alone, 2025 saw \

$111 billion in new scale-up funding, 93% of which went to AI-focused firms . To put it starkly,

“for every dollar invested in technology, 93 cents flow into AI”

. Crunchbase reports that all major

late-stage rounds in 2023 went to a few “foundation model” companies: OpenAI, Anthropic,

Inflection, etc. . Even after record 2023 fundraising, AI funding remained robust in early 2024,

reflecting high investor commitment.

Private Company Valuations

Tens of hundreds of private AI companies now carry nine-figure

or higher valuations. Examples cited by analysts include: Safe Superintelligence (ex-OpenAI team)

raising \$2B at ~\$32B valuation, Thinking Machines Lab (ex-OpenAI lead) raising \$2B at \ $12B .

Fortune 500 firms are so eager they hunt for AI consultants just to signal participation . The

result: “unicorns” (startups >\$1B) numbering in the many hundreds. In fact, one report notes

nearly 500 AI-focused startups exceed \$1B valuations (avg \$5.4B), and 1,300 exceed \$100M,

often without meaningful revenue .

Public Market Performance

Beyond Nvidia, broad market indices are heavily influenced by AI

optimism. The top tech stocks (the “Magnificent Seven” including Nvidia, Apple, Microsoft,

Amazon, Alphabet, Meta, Tesla) collectively gained enormous weight in 2023–25. The U.S. market

added about \$21 trillion in value since late 2022, with only ten firms (mostly AI-centric)

contributing 55% of that increase . For example, Nvidia and Microsoft each saw ~30–60% stock

price rises in months after the ChatGPT debut . In early 2025, U.S. tech investment powered all

GDP growth.

Valuation Multiples

Analysts flag sky-high P/E ratios. One chart (Slok) shows today’s top 10 S&P

500 firms have P/Es well above late-1990s bubble levels . An AI-focused stock index trades

around 30× expected earnings; dot-com era internet stocks peaked ~25×

. This disparity suggests

the market is pricing in extremely rapid future growth. (For reference, Nvidia’s forward P/E in

mid-2025 was ~30, below its recent average , reflecting confidence, but also the high benchmark

set by itself.)

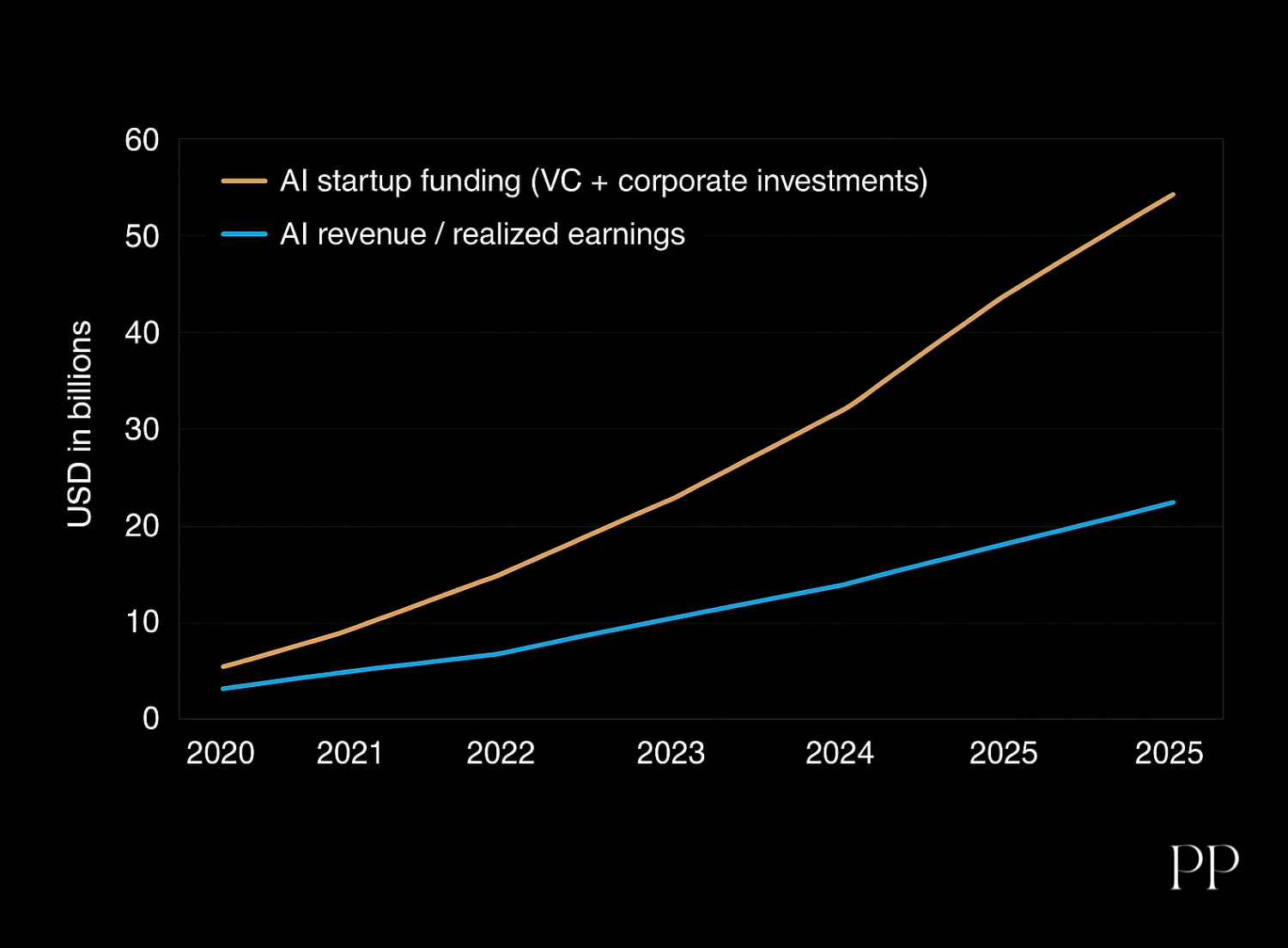

AI Investment vs. AI Revenue

In Summary

Investment data reveal extreme inflation of AI-related asset prices, reminiscent of

bubble conditions. Ultra-low interest rates have further fueled capital availability, meaning many AI

projects get financed even without proven business plans. That said, some of the investment is into core

AI infrastructure (chips, data centers) that will persist as technology building blocks, blurring the line

between speculation and long-term investment.

Media Narratives and Public Hype

Public discourse has been saturated with AI hype. Leading tech figures and press have often presented

AI breakthroughs as revolutionary and inevitable:

Corporate Hype

CEOs proclaim AI milestones grandly. For example, Google’s Sundar Pichai said

large language models (LLMs) are “more profound than fire,

” and AI pioneer Geoffrey Hinton

compared them to electricity or the Industrial Revolution . Such statements create powerful newera narratives. Firms scramble to board the train: one analysis noted companies that added “AI”

to their name saw immediate stock bumps . Earnings calls and analyst notes routinely emphasize

AI as a key growth driver.

Consultant and Analyst Claims

The McKinsey and Morgan Stanley reports exemplify megahype: McKinsey estimated a \$2.6–4.4 trillion annual productivity gain from generative AI , while

Morgan Stanley projected a \$6 trillion AI opportunity. (Notably, these firms also offer paid

consulting, illustrating the hype-feedback loop .) Venture advisors warn executives not to “fall

behind,

” pushing widespread corporate AI pilots regardless of readiness.

Media Sensationalism

Tech media and mainstream outlets frequently pose alarm or aweridden questions (e.g.

“Is AI going to replace all our jobs?”). Articles often highlight the

possibilities of AI—potential new industries, autonomous cars, AI doctors—without always

tempering expectations. The Economist noted that AI firms in the West earn only ~$50 billion/

year now, whereas companies are investing trillions . Outlets also amplify warning voices: recent

headlines point out that some hedge funds see an echo of dot-com telecom gluts, and that UBS’s

research finds AI firm revenues lagging the cost of building infrastructure.

Hype Cycle Patterns

Experts on technology hype note familiar patterns. A Harvard/Kennedy

essay observes “every business tried to become an AI business” in early 2023 , and that even

asking “learn AI” became boilerplate in news stories and ads. The early AI frenzy mirrors past

tech waves (steam, auto, electricity) where adoption was presented as indispensable . However,

such narratives often gloss over AI’s limitations: Cambridge researcher Kerry McInerney points

out AI’s promised abilities (“seeing trends in data”) are routinely overstated and often misleading

. Thus, the “media narrative” component of hype is that magical framing which may not align

with current reality.

Overall

public perception is polarized Early on, enthusiasm was nearly unbridled; more recently,

stories of AI’s shortcomings and high costs (especially of gen-AI data centers) have begun to surface.

This clash fuels debate: some see a world-changing revolution, while others see a classic case of

overpromising.

Expert Opinions and Commentary

A variety of authorities have weighed in on the bubble question:

Economists

Many financial experts now openly raise bubble alarms. Gary Smith (Pomona

College) asserts that AI stocks are repeating the dot-com pattern: overpriced “story stocks”

detached from earnings. Similarly, Torsten Slok (Apollo Global) calls today’s valuations more

extreme than 1999’s . UBS analysts and hedge funds have noted AI firm valuations leave “little

room for cash-flow disappointments”

. Overall, their consensus is that a corrective risk is real if

AI revenues don’t materialize as hoped.

Venture Investors

Within tech investing, views differ. Some top VCs are warning of excess.

OpenAI’s Sam Altman has candidly said the industry is in a bubble: it’s “not rational” that

startups with “three people and an idea” fetch massive sums . Others (often holding equity in AI

companies) remain bullish. For example, in 2025 Macro investor Jordi Visser argued that not only

is AI not a bubble, but it is the only investment theme worth loading up on . He points to

accelerating demand for AI (Oracle’s stock jumped on a \$400B backlog, he notes) as evidence

that fundamentals will justify valuations.

AI Researchers

Many in the research community urge caution. The Allen Lab authors (Widder &

Hicks) trace the “hype cycle” and warn of “harmful effects” if companies oversell generative AI .

They emphasize that, historically, technologies were often oversold before proving their worth

(e.g. IBM’s Watson in healthcare). Scholars like Kerry McInerney highlight the overpromising

problem: attributing “magical powers” to AI that current systems don’t actually possess . Even in

policy circles, figures like Milton Mueller argue that hyperbolic narratives (“superintelligence”

,

“God-like AI”) distort understanding and policymaking.

Market Analysts

Some prominent investors compare the situation to past manias. For

example, hedge fund Praetorian Capital warned “Global Crossing is reborn” under current AI

hype. Tech commentator Ed Zitron likened it to the 2007 subprime bubble, noting that like cheap

Chinese AI models in early 2024 triggered trillion-dollar stock sell-offs. These voices underscore

the parallels to previous bubbles.

In Short

Many experts see clear bubble signals (extreme valuations, hyperbole, potential disconnect

from profits). A smaller set of investors argue the market is merely pricing in a massive technological

shift. The range of opinions reflects the genuine uncertainty: a true bubble may only be declared once it

bursts or permanently sows losses.

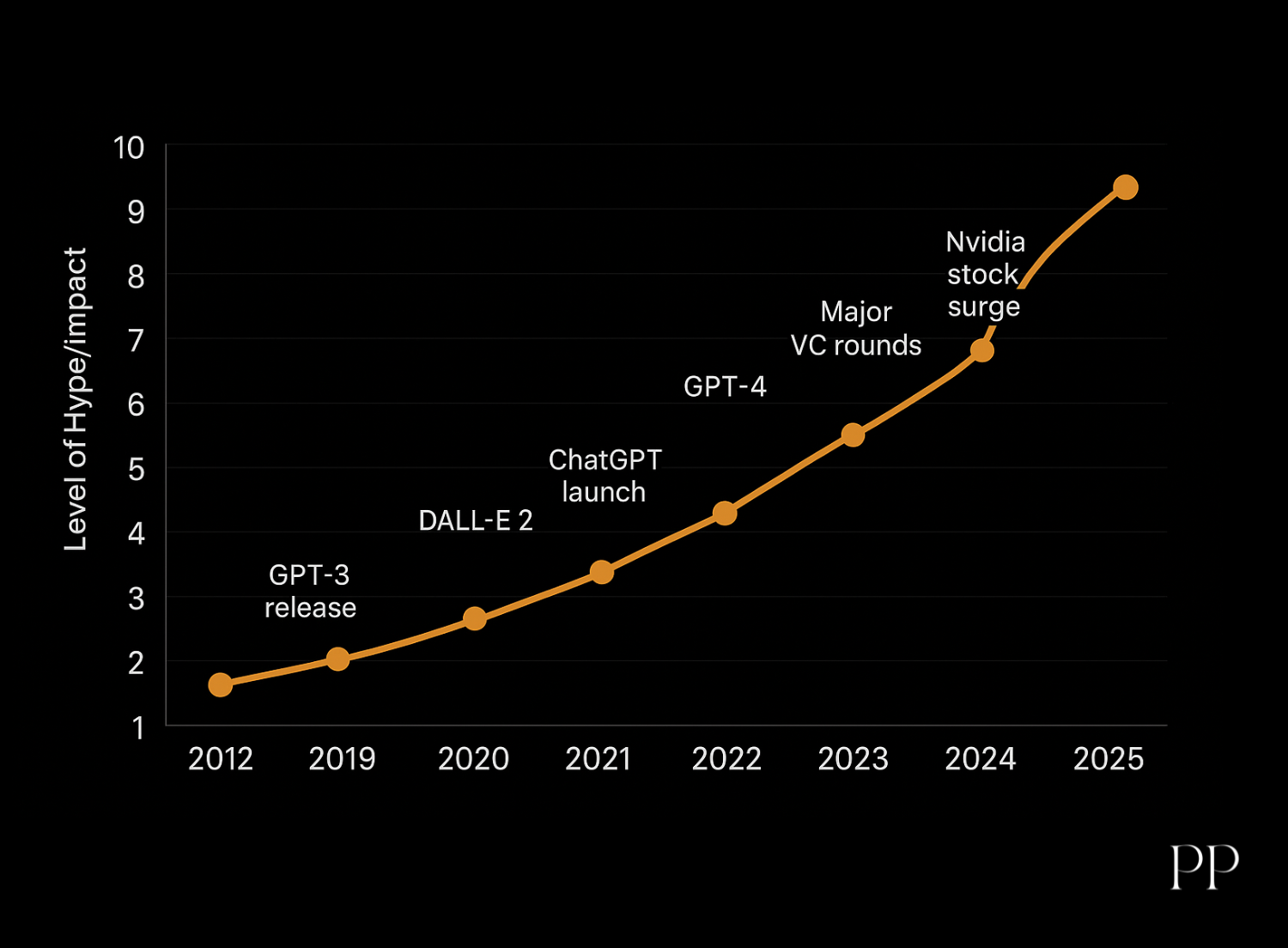

Timeline: Key AI Inflection Points

2012–2017: Deep learning breakthroughs (e.g. ImageNet 2012, AlphaGo 2016) sowed early AI

enthusiasm, but funding remained modest.

June 2020: OpenAI unveils GPT-3 (175B parameters), generating massive attention . It powers new NLP

applications, hinting at AI’s potential scale.

April 2021: DALL·E 2 image generator showcases AI artistry, sparking viral demos (not directly cited

here).

Nov 2022: OpenAI releases ChatGPT to the public. It instantly goes viral – drawing ~100 million users

within two months – and forces tech giants to respond.

Feb 2023: Google rolls out Bard, Meta and Amazon unveil competing tools, as the so-called AI “arms

race” begins.

Mar 14, 2023: OpenAI drops GPT-4 suddenly . Its multimodal (image+text) capabilities and broader

knowledge dramatically improve on ChatGPT, reinvigorating excitement.

Jan 2023: Microsoft announces a new multiyear partnership with OpenAI (part of an intended ~$10B

investment) . (OpenAI’s prior backs included Microsoft’s \$1B in 2019.)

2023 (Remainder): Funding rounds surge: Anthropic raises multiple billions (including Amazon’s \$4B

deal in late 2023) , Inflection and others close mega-rounds. Traditional VCs funnel record capital into AI

startups.

Oct 2023: OpenAI reportedly closes a \$6.6B round, valuing the company around \$150–160B . This

and other data cement the narrative of an AI investment boom.

Jan 2025: Anthropic raises \$2B at a \$60B valuation , compared to its \$18B valuation in 2024.

Similarly large financings continue (e.g. xAI, Adept).

Jul 2025: Nvidia’s stock caps a run-up by reaching \$4T market value , the first firm ever to hit that

mark.

Sep 2025: Anthropic more than doubles its valuation to \$183B after a \$13B funding round .

PitchBook notes AI startups drive a surge in overall VC funding (U.S. funding jumped 75% H1 2025

largely due to AI) .

This timeline shows an accelerating pace: within 2–3 years AI went from lab demos to products and

enormous capital allocations, faster than the dot-com era. Each key event (GPT releases, ChatGPT going

mainstream) has been an inflection point, fueling the next phase of funding and media attention.

Timeline: Key AI Inflection Points

Aspect

Historical Bubble (e.g. Dot-Com)

Current AI Boom

Valuation Spike

NASDAQ up ~600% (1995–2000), then crash.

Magnificent Seven stocks +1500% (since 2020) (Nvidia up ~700% since ChatGPT).

Funding Frenzy

Y2K-era investments in web portals, fiber, telco (often no profits).

$80–100B+ annually into AI startups (2023–25).

Media Narrative

“New economy”, endless growth stories; many IPOs on hype.

“AI is the new electricity”; leaders call it revolutionary.

Fundamentals

Many dot-coms had no revenue; few business cases succeeded.

AI infrastructure (chips, cloud) generates real revenue; some AI applications profitable (e.g. AI APIs, semiconductor chips) – but most frontier AI firms are not yet profitable.

Market Structure

Numerous small tech IPOs (telecom boom).

Concentrated: a few giants (Nvidia, Google, Microsoft, Meta, Amazon) lead AI stocks, with hundreds of private startups behind.

P/E Ratios

Top tech P/Es ~20–25× in late-’90s.

Top AI/tech P/Es ~30× or more. Slok: S&P tech leaders are “more overvalued” than in 1999.

Signs of strain are emerging (projected 2025 datacenter spending vs. current revenues). Some AI stocks have dipped on mixed results. But central bank policy and earnings effects are still uncertain.

Like prior bubbles, today’s AI hype was stoked by stories and optimism. Investors, fearing to miss out,

have often treated new AI ideas as must-buy propositions . Anecdotes abound of companies rebranding

as “AI”

. The market’s behavior exhibits greater-fool dynamics: paying high prices in hope of selling to

someone else at an even higher price. Gary Smith explicitly warns that absent clear profits, buyers are

simply “embracing the Greater Fool Theory”

.

Nevertheless, some note differences. Dot-coms in 2000 largely delivered no lasting value (indeed many

died), whereas today’s AI infrastructure may be a genuine platform shift. The “boom” advocates argue

we might be witnessing a foundational technology that will reshape multiple industries. If so, the line

between “bubble” and “growth boom” is blurred. However, prudent analysts emphasize that

expectations are astronomically high. OpenAI’s CEO Sam Altman himself confirms,

“Are we in a phase

where investors as a whole are overexcited about AI? … My opinion is yes”

.

In Conclusion

AI exhibits both familiar bubble traits and elements of genuine tech evolution. Data from

connected sources paint a vivid picture: unprecedented investment levels and sky-high valuations stand

in stark contrast to current profit realization . Whether this ends in a sharp correction or a measured

maturation remains to be seen. What is clear is that the AI era, like past booms, will leave lasting

impacts—positive and negative—depending on how carefully enterprises, investors, and policymakers

navigate the hype and reality.

Sources: Academic analyses of bubbles ; historical records of the dot-com boom ; venture funding and valuation data ; media reports

and expert commentary.