U.S. Services Sector Faced Heightened Inflation in March

Image Credit : Bloomberg

Source Credit : Portfolio Prints

U.S. services sector growth slowed in March, while the cost of business inputs surged at the fastest pace in more than 13 years—an early signal that the prolonged conflict with Iran is intensifying inflation pressures.

Data released Monday by the Institute for Supply Management also showed services employment falling to its lowest level since late 2023. However, that weakness appears somewhat at odds with official government data released last week, which pointed to a strong rebound in overall job growth.

The Middle East conflict, now in its second month, dominated business sentiment in the survey. Companies across sectors—from construction to wholesale trade—flagged rising uncertainty tied to the war. Even before the conflict, firms were grappling with volatility linked to import tariffs.

The report reinforces expectations that the Federal Reserve will keep interest rates on hold in the near term.

“The service sector is still expanding, but headwinds are building,” said Priscilla Thiagamoorthy, senior economist at BMO Capital Markets. “Softening employment alongside renewed price pressures points to slower growth with persistently high inflation, leaving the Fed in a difficult position.”

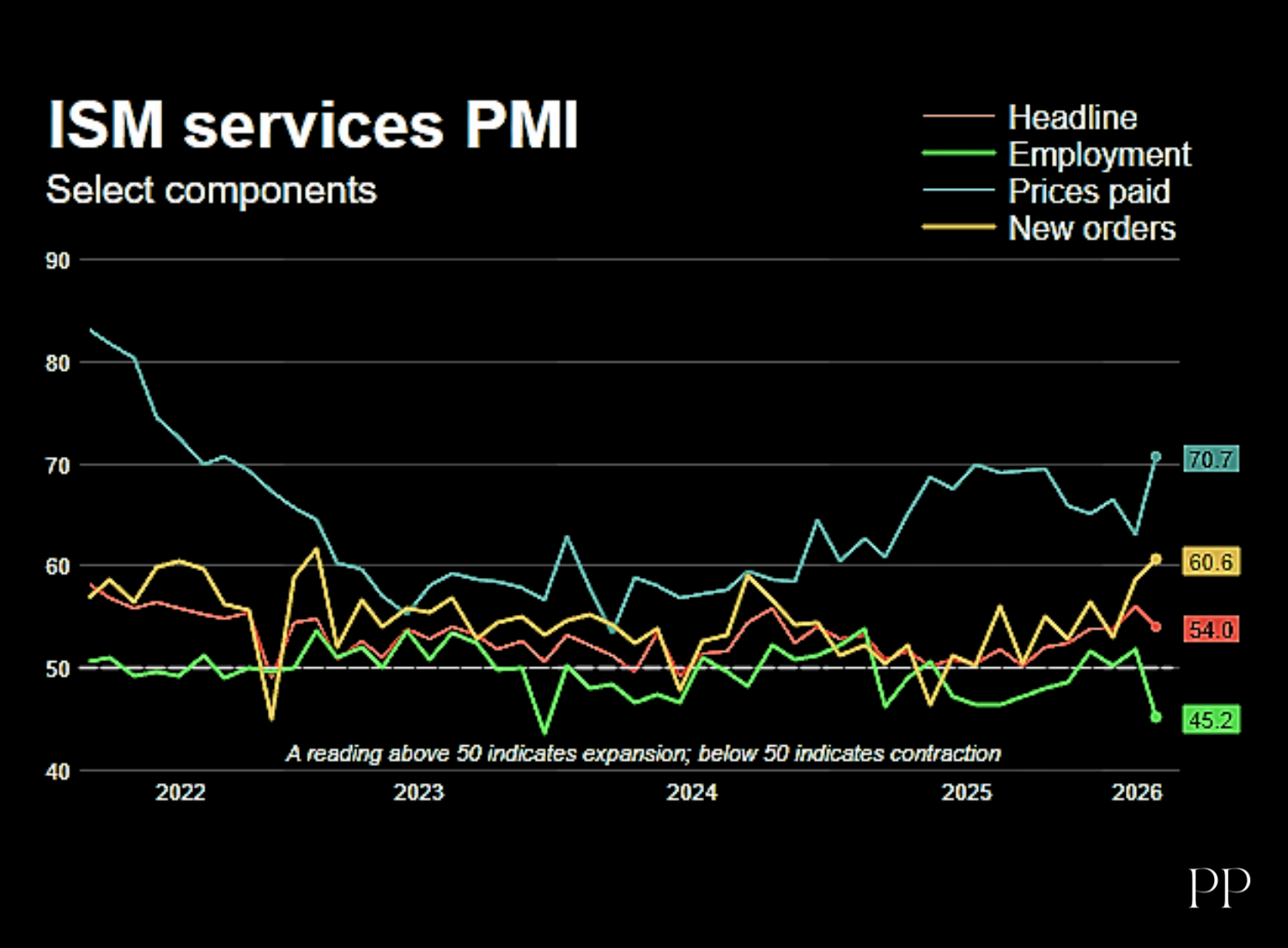

The ISM’s nonmanufacturing purchasing managers’ index (PMI) slipped to 54.0 in March from 56.1 in February, below economists’ expectations of 54.9. A reading above 50 indicates expansion in the services sector, which accounts for more than two-thirds of U.S. economic activity.

Thirteen industries—including wholesale trade, transportation and warehousing, mining, construction, and utilities—reported growth. Meanwhile, retail trade, agriculture, and public administration contracted. Some mining firms cited reduced international business due to political uncertainty surrounding the Iran conflict.

Businesses in real estate and leasing said the war has compounded an already fragile macroeconomic environment. Wholesalers pointed to rising logistics costs, citing threats to close the Strait of Hormuz and increasing war-risk surcharges—even affecting air freight.

The conflict has driven global oil prices up by more than 50%, pushing U.S. gasoline prices above $4 per gallon for the first time in nearly four years. Economists expect these pressures to show up in upcoming inflation data, including the March Consumer Price Index.

Producer prices had already surged in February in anticipation of escalating tensions, with shipping disruptions through the Strait of Hormuz affecting a wide range of goods, from energy to fertilizers.

As a result, expectations for interest rate cuts this year have diminished significantly. The Federal Reserve last month kept its benchmark rate unchanged in the 3.50%–3.75% range.

Financial markets showed limited reaction. Wall Street stocks edged higher, the dollar was broadly stable, and U.S. Treasury yields remained steady.

The ISM’s measure of prices paid jumped sharply by 7.7 points to 70.7—the highest level since October 2022 and the largest monthly increase in over 13 years. The index has now remained above 60 for 16 consecutive months, underscoring persistent cost pressures.

“Companies across multiple industries are reporting higher fuel costs and building inventories to guard against supply disruptions,” said Steve Miller, chair of the ISM Services Business Survey Committee. He added that construction materials such as lumber, copper, and steel are also becoming more expensive.

Trade policy uncertainty continues to add to business concerns. Although tariffs introduced under Donald Trump were struck down by the U.S. Supreme Court, new global tariffs have been imposed for up to 150 days.

Wholesalers reported a significant rise in landed costs, while businesses in accommodation and food services noted that shifting tariff policies—despite some rollbacks—continue to fuel uncertainty.

The survey’s supplier deliveries index rose to 56.2 from 53.9, indicating slower delivery times. This trend mirrors delays seen in the manufacturing sector, driven by supply chain disruptions and logistical bottlenecks.

Some businesses cited backlogs from suppliers and manufacturers, while others pointed to truck shortages as a key constraint on deliveries.

New orders rose to a two-year high of 60.6, though export growth slowed and the increase in backlogs moderated, suggesting mixed momentum in demand.

Employment in the services sector declined, with the ISM jobs index dropping to its lowest level since December 2023. However, this contrasts with government data showing a strong rebound in payrolls, including a 143,000 increase in private service-sector jobs.

Economists caution that the ISM employment index is not always a reliable predictor of official labor market data.

“The employment drop would be more concerning if not for the strong payrolls data,” said John Ryding, chief economic advisor at Brean Capital. “But the sharp rise in prices paid is a clear warning sign and suggests inflation could remain close to 4%, which will concern the Fed.”

Thirteen industries—including wholesale trade, transportation and warehousing, mining, construction, and utilities—reported growth. Meanwhile, retail trade, agriculture, and public administration contracted. Some mining firms cited reduced international business due to political uncertainty surrounding the Iran conflict.

Businesses in real estate and leasing said the war has compounded an already fragile macroeconomic environment. Wholesalers pointed to rising logistics costs, citing threats to close the Strait of Hormuz and increasing war-risk surcharges—even affecting air freight.

The conflict has driven global oil prices up by more than 50%, pushing U.S. gasoline prices above $4 per gallon for the first time in nearly four years. Economists expect these pressures to show up in upcoming inflation data, including the March Consumer Price Index.

Producer prices had already surged in February in anticipation of escalating tensions, with shipping disruptions through the Strait of Hormuz affecting a wide range of goods, from energy to fertilizers.

As a result, expectations for interest rate cuts this year have diminished significantly. The Federal Reserve last month kept its benchmark rate unchanged in the 3.50%–3.75% range.

Financial markets showed limited reaction. Wall Street stocks edged higher, the dollar was broadly stable, and U.S. Treasury yields remained steady.

The ISM’s measure of prices paid jumped sharply by 7.7 points to 70.7—the highest level since October 2022 and the largest monthly increase in over 13 years. The index has now remained above 60 for 16 consecutive months, underscoring persistent cost pressures.

“Companies across multiple industries are reporting higher fuel costs and building inventories to guard against supply disruptions,” said Steve Miller, chair of the ISM Services Business Survey Committee. He added that construction materials such as lumber, copper, and steel are also becoming more expensive.

Trade policy uncertainty continues to add to business concerns. Although tariffs introduced under Donald Trump were struck down by the U.S. Supreme Court, new global tariffs have been imposed for up to 150 days.

Wholesalers reported a significant rise in landed costs, while businesses in accommodation and food services noted that shifting tariff policies—despite some rollbacks—continue to fuel uncertainty.

The survey’s supplier deliveries index rose to 56.2 from 53.9, indicating slower delivery times. This trend mirrors delays seen in the manufacturing sector, driven by supply chain disruptions and logistical bottlenecks.

Some businesses cited backlogs from suppliers and manufacturers, while others pointed to truck shortages as a key constraint on deliveries.

New orders rose to a two-year high of 60.6, though export growth slowed and the increase in backlogs moderated, suggesting mixed momentum in demand.

Employment in the services sector declined, with the ISM jobs index dropping to its lowest level since December 2023. However, this contrasts with government data showing a strong rebound in payrolls, including a 143,000 increase in private service-sector jobs.

Economists caution that the ISM employment index is not always a reliable predictor of official labor market data.

“The employment drop would be more concerning if not for the strong payrolls data,” said John Ryding, chief economic advisor at Brean Capital. “But the sharp rise in prices paid is a clear warning sign and suggests inflation could remain close to 4%, which will concern the Fed.”